Author: Javeed Dhillon | Reviewed by: Licensed Mortgage Professional | Last Updated: May 2026

Sources: HUD Single Family Housing Policy Handbook 4000.1 | FHA.gov | HUD Mortgagee Letters 2023–2026 | HMDA Data 2024

What you’ll learn: Exactly what an FHA loan is, what it costs in 2026, who qualifies, what lenders actually look for (not what they publicly state), and how to choose the right loan for your situation — with a decision framework at the end.

What Is an FHA Loan?

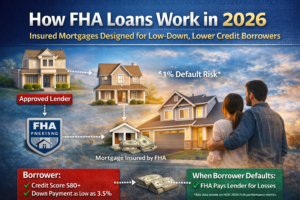

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA), a government agency under the U.S. Department of Housing and Urban Development (HUD). The FHA doesn’t lend money — it insures loans made by private lenders, which means if you default, the government compensates the lender.

That guarantee is what allows lenders to approve borrowers they’d otherwise reject. Lower credit scores. Smaller down payments. Higher debt loads. FHA loans exist specifically for people who can’t yet qualify for conventional financing.

Since 1934, the FHA has insured over 50 million mortgages, making it the largest residential mortgage insurer in the world.

FHA Loan requirements 2026

(Per FHA Single Family Housing Policy Handbook 4000.1, current as of May 2026)

Credit Score

| Credit Score | Minimum Down Payment |

| 580 or higher | 3.5% |

| 500 – 579 | 10% |

| Below 500 | Not eligible |

What lenders won’t tell you upfront: The FHA minimum is 500, but most lenders impose what’s called a lender overlay — their own internal minimum, typically 580–620. Some even require 640. Shop at least three lenders before assuming you don’t qualify. One lender’s “no” is often another’s “approved.”

Also important: your credit score isn’t just a number. Lenders review the full credit file — late payments in the past 12 months, charge-offs, collection accounts, and the age of your credit history. Two borrowers with a 600 score can get very different outcomes depending on what’s behind that number.

Down Payment

Minimum 3.5% with a 580+ credit score, 10% with a 500–579 score. There is no zero-down FHA option, despite what some ads imply. The FHA sets the maximum loan-to-value (LTV) ratio at 96.5%.

Allowed down payment sources (per HUD Handbook 4000.1, Section II.A.3):

- Personal savings (bank accounts, investment accounts, retirement funds with withdrawal documentation)

- Gift funds from family, close friends, employer, or charitable organizations (with a signed gift letter — no repayment implied)

- Down payment assistance (DPA) programs offered by state housing finance agencies

- Seller concessions — up to 6% of the purchase price can cover closing costs (not the down payment itself)

Common myth: Gift funds must be “seasoned” in your account for 60 days. This is false. If you can document the source of the gift with bank statements and a gift letter, lenders must accept it — regardless of when it landed in your account. This myth originated from conventional loan rules and gets incorrectly applied to FHA.

Debt-to-Income Ratio (DTI)

FHA guidelines allow:

- Front-end ratio (housing only): up to 31% of gross monthly income

- Back-end ratio (all debt): up to 43% of gross monthly income

- With compensating factors: up to 50% back-end DTI

Compensating factors that can push DTI to 50% include:

- 12 months of cash reserves after closing

- No increase in housing costs (“payment shock” below 5%)

- Residual income above FHA threshold

- Additional non-documented income

Real example: Monthly gross income of $5,500. Proposed mortgage of $1,550. Car payment of $350. Credit card minimums of $125. Total monthly debt = $2,025. Back-end DTI = 36.8%. Well within FHA limits.

Employment and Income

- Minimum two years of employment history (same field — employer can change)

- Self-employed borrowers: two years of tax returns showing consistent income; lenders average the two years

- Part-time income counts if documented for two years

- Rental income, child support, disability, and pension all qualify with proper documentation

Insider note on self-employed borrowers: If your business had a strong 2024 and a weaker 2025, the lender will average both years — even if 2026 is your best year yet. If you’re self-employed, the timing of your application matters as much as your income.

Property Requirements

The home must pass an FHA appraisal — a two-in-one review that assesses both market value and property condition against HUD’s Minimum Property Standards (MPS).

Common FHA appraisal deal killers:

- Peeling or chipping paint (especially in pre-1978 homes, due to lead paint regulations)

- Roof with less than two years of remaining life

- Missing handrails on staircases

- Broken windows or doors

- Standing water in crawl spaces or basement

- Non-functional HVAC, plumbing, or electrical systems

- Signs of pest infestation (visible damage or frass)

- Unsafe access to the property

Why sellers sometimes reject FHA buyers: If a seller knows their home needs $8,000 in repairs to pass an FHA appraisal, they’d rather take a conventional buyer who doesn’t trigger that scrutiny. This is a real market dynamic in 2026, especially in competitive metros. If you’re using FHA financing, consider writing an offer on homes that are newer, well-maintained, or clearly move-in ready.

Additional Requirements

- Must be your primary residence (you must move in within 60 days of closing)

- One FHA loan at a time (with narrow exceptions — relocation, expanding family, co-borrowers)

- No FHA foreclosure in the past three years

- Chapter 7 bankruptcy: must be discharged at least two years, with re-established credit

- Chapter 13 bankruptcy: eligible after one year of on-time payments with court approval

FHA Loan Limits 2026

(Effective January 1, 2026 — Source: HUD Mortgagee Letter setting 2026 FHA limits)

HUD adjusts loan limits annually based on median home prices by county. For 2026:

| Property Type | Standard Areas | High-Cost Areas |

| Single-family home | $541,287 | $1,249,125 |

| 2-unit property | $693,000 | $1,600,050 |

| 3-unit property | $837,750 | $1,934,100 |

| 4-unit property | $1,040,625 | $2,403,900 |

Special higher limits apply in Alaska, Hawaii, Guam, and the U.S. Virgin Islands due to elevated construction costs.

Practical impact: In most midwestern and southern markets, the $541,287 limit is more than enough. In high-cost metros like Los Angeles, New York, or Seattle, you may find that your target home’s price exceeds even the high-cost FHA limit — in which case, conventional jumbo financing is your only option.

FHA Mortgage Insurance Premium (MIP) — The Real Cost

This is the piece most articles gloss over. Let’s be precise.

FHA MIP in 2026 has two components:

-

Upfront MIP (UFMIP)

- Rate: 1.75% of the loan amount

- Paid at closing or rolled into the loan balance

- On a $300,000 loan: $5,250

-

Annual MIP (Paid Monthly)

- Standard rate for most borrowers in 2026: 0.55% annually

- Full rate table (per HUD Mortgagee Letter 2023-05, rates unchanged through 2026):

| Loan Term | LTV | Annual MIP Rate |

| 30 years | > 95% (< 5% down) | 0.55% |

| 30 years | ≤ 95% (≥ 5% down) | 0.50% |

| 15 years | > 90% | 0.40% |

| 15 years | ≤ 90% | 0.15% |

Monthly MIP calculation:

Loan amount × annual MIP rate ÷ 12

$300,000 × 0.55% ÷ 12 = $137.50/month

How Long Does MIP Last?

| Down Payment at Closing | MIP Duration |

| Less than 10% | Entire loan term (30 years) |

| 10% or more | 11 years |

This is fundamentally different from conventional PMI, which cancels automatically when you reach 20% equity. FHA MIP does not cancel based on equity — only based on down payment percentage and time.

Removing FHA MIP — Your Exit Strategies

Option 1: Refinance into a conventional loan

Once you have 20% equity (combination of down payment, principal paydown, and appreciation), refinance. You eliminate MIP entirely and potentially get a better rate. Most FHA borrowers do this within 5–8 years.

Option 2: Make a 10%+ down payment upfront

MIP drops off after 11 years. Only makes sense if you plan to hold the loan long-term.

Option 3: FHA Streamline Refinance

If rates drop, refinance into a new FHA loan with minimal documentation. You’ll get a partial refund on your UFMIP if done within three years. The refund percentage decreases each month.

FHA vs. Conventional vs. VA vs. USDA — Full Comparison

| Feature | FHA | Conventional | VA | USDA |

| Min. Credit Score | 500 | 620 | 580+ | 640 |

| Min. Down Payment | 3.5% | 3–20% | 0% | 0% |

| Mortgage Insurance | MIP (required) | PMI (if < 20%) | Funding fee | Guarantee fee |

| MI Cancelable? | No (mostly) | Yes (at 20% equity) | N/A | No |

| Loan Limits | Up to $1,249,125 | Up to $1,249,125 | None (conforming) | None (rural areas) |

| Property Type | Primary only | Any | Primary only | Primary, rural only |

| Eligible Borrowers | All | All | Veterans/Active duty | Low-income, rural |

| DTI Limit | Up to 50% | Typically 43–45% | 41% guideline | 41% guideline |

Bottom line:

- VA loan is always better than FHA if you’re eligible (no MI, no down payment, better rates)

- USDA loan is better in rural areas if income qualifies (zero down, low fees)

- FHA is the strongest option for non-veterans in urban/suburban markets with lower credit or savings

- Conventional wins long-term if your credit score is 700+ and you can hit 20% down

FHA Loan vs. Conventional Loan — Side by Side (2026)

(Based on Bankrate national rate averages, February 2026)

| FHA | Conventional | |

| Average 30-year rate | ~6.16% | ~6.09% |

| APR (including MI costs) | Higher | Lower (with 20% down) |

| Monthly MI on $300K | $137.50 | $0 (with 20% down) |

| Total MI cost over 30 yrs | ~$49,500 | $0 (with 20% down) |

| Break-even point | — | ~7 years (with 10% conventional down) |

Critical nuance: Conventional PMI rates for borrowers with 620–680 credit scores are actually higher than FHA MIP. At a 640 credit score, conventional PMI can run 1.5–2.0% annually, versus FHA’s flat 0.55%. For lower-credit borrowers, FHA often wins on total monthly cost — even with lifetime MIP.

Types of FHA Loans Available in 2026

FHA 203(b) — Standard Purchase Loan

The default program. Used for purchasing or refinancing a 1–4 unit primary residence. Requires fixed or adjustable rate.

FHA 203(k) Rehabilitation Loan

Finance the purchase AND renovation in one mortgage. Two versions:

- Standard 203(k): Major structural repairs, additions, renovation — minimum $5,000 in repairs, no upper cap (within loan limits)

- Limited 203(k): Cosmetic and non-structural repairs — up to $35,000

Hidden complexity: 203(k) loans require a HUD-approved 203(k) Consultant for Standard loans. They’re slower to close (45–60 days minimum), and not every FHA lender offers them. Many borrowers start with a standard FHA purchase and later do an FHA cash-out refi for renovations — often simpler.

FHA Streamline Refinance

Existing FHA borrowers only. Reduced documentation, no appraisal required in most cases. Net tangible benefit required — typically a 5% reduction in principal + interest + MIP.

FHA Cash-Out Refinance

Access up to 80% of your home’s appraised value in cash. Credit, income, and employment verification required. Cannot exceed FHA loan limits.

FHA Reverse Mortgage (HECM)

For homeowners 62+. Converts equity to cash with no monthly mortgage payments. Repaid when the borrower sells, moves, or passes away. Regulated and insured by the FHA.

FHA One-Time Close Construction Loan

Finances construction + permanent mortgage in one loan with one closing. Eliminates the need for a separate construction loan and a second closing.

FHA Condo Loans — A Common Trap

You can buy a condo with an FHA loan, but the entire condo project must be FHA-approved. As of 2026, fewer than 10% of U.S. condo developments are on the FHA approved list. Before falling in love with a condo, check HUD’s condo approval database. If the project isn’t approved, your FHA loan won’t work — period. You’d need to pursue Single Unit Approval (SUA) for an individual unit, which requires the building to meet specific HOA reserve and owner-occupancy criteria.

How to Apply for an FHA Loan — Step by Step

Step 1: Pull Your Credit Reports

Get all three bureau reports free at AnnualCreditReport.com. Dispute inaccuracies — even a minor error on a credit limit or balance can suppress your score. Give yourself 30–45 days to clear disputes before applying.

Step 2: Calculate Your True Budget

Use gross monthly income, not take-home pay. DTI calculations always use gross.

Quick DTI check:

- Add all monthly minimum debt payments

- Divide by gross monthly income

- If above 43%, address debts before applying; if 43–50%, you may still qualify with compensating factors

Step 3: Shop Multiple FHA Lenders

The FHA sets the floor — lenders set the price. On a $300,000 loan, a 0.25% rate difference is $45/month. Over 30 years, that’s $16,200. Shopping three lenders takes two hours. That’s the math.

Get Loan Estimates from at least three FHA-approved lenders. Compare:

- Interest rate

- APR (includes fees)

- Origination fees

- Third-party closing costs

- Rate lock terms

Step 4: Get Pre-Approved (Not Pre-Qualified)

Pre-qualification is a guess. Pre-approval involves actual credit pull and income verification — it’s what sellers and their agents respect in 2026’s competitive market. Get a Certified Approval if your lender offers it — underwriting done upfront, which makes your offer as strong as a cash offer.

Step 5: Find a Home That Will Pass the FHA Appraisal

Tell your real estate agent you’re using FHA financing. Target homes built after 1978 (no lead paint requirement), with functioning systems and no visible deferred maintenance. The FHA appraisal will flag anything a lender wouldn’t want to see.

Step 6: Lock Your Rate at the Right Time

Rate locks typically run 30–60 days. Lock too early and you risk paying for an extension. Lock too late and you risk rate movement before closing. Your lender will advise based on the timeline.

Step 7: FHA Appraisal and Underwriting

The FHA appraiser is assigned by the lender through an AMC (Appraisal Management Company) — you cannot request a specific appraiser. If the appraisal comes back below purchase price, you can:

- Renegotiate the price with the seller

- Pay the difference in cash (loan amount can’t exceed appraised value)

- Walk away (FHA loans include an appraisal contingency)

Underwriting reviews your complete file: income docs, assets, credit, property. Expect requests for additional documentation (called “conditions”). Respond quickly — every delay from your side can push closing.

Step 8: Close

Review your Closing Disclosure 3 business days before closing. Compare it to your Loan Estimate. Question any fee increases. On closing day: bring a cashier’s check or wire funds for closing costs and down payment. Sign. Get keys.

Best FHA Lenders 2026 — What to Look For

We’re not listing specific lender names here because rates and service quality change constantly. Instead, here’s what separates strong FHA lenders from average ones:

What a strong FHA lender looks like:

- Specializes in government-backed loans (FHA, VA, USDA) — not a sideline product

- Offers manual underwriting for borderline borrowers

- Has in-house underwriting (faster turnarounds, better communication)

- Transparent on lender overlays (tell you upfront, not after pulling credit)

- Competitive origination fees (below 1% of loan amount)

- Experience with 203(k), condo SUA, and self-employed borrowers if applicable

Where to find FHA-approved lenders: HUD.gov maintains a searchable database of FHA-approved lenders by state. Credit unions often have fewer overlays and lower fees than large retail banks. Mortgage brokers can access multiple FHA lenders simultaneously.

FHA Closing Costs — What to Expect

FHA closing costs typically run 2.5%–5% of the loan amount. On a $300,000 loan: $7,500–$15,000.

Common FHA closing costs:

| Cost | Typical Range |

| Origination fee | 0.5%–1% of loan |

| FHA appraisal | $400–$700 |

| Title insurance | $500–$1,500 |

| Title search | $200–$400 |

| Attorney fee (where required) | $500–$1,000 |

| Home inspection | $300–$500 |

| Survey | $150–$400 |

| Prepaid interest | Varies by closing date |

| Escrow setup (taxes + insurance) | 2–3 months reserves |

| Recording fees | $50–$250 |

| Upfront MIP (1.75%) | $5,250 on $300K loan |

Can the seller pay FHA closing costs?

Yes. The FHA allows seller concessions of up to 6% of the purchase price toward closing costs. In buyers’ markets, this is negotiable. In hot markets, sellers rarely agree. In 2026’s inventory-constrained environment, don’t count on seller credits in competitive bidding situations — but always ask.

Can closing costs be rolled into the loan?

The upfront MIP (1.75%) can be rolled in. Standard closing costs generally cannot exceed the appraised value limitation and aren’t rolled into purchase loans. However, in a refinance, closing costs can often be financed.

FHA Appraisal Red Flags — What Can Kill Your Deal

These are the issues that most commonly cause FHA appraisals to fail, based on HUD’s Minimum Property Standards (HUD Handbook 4000.1, Section II.A.3.d):

- Peeling, chipping, or flaking paint — on any surface of homes built before 1978; lender must require repair before closing

- Roof condition — appraiser estimates remaining useful life; less than two years typically triggers repair requirement

- Foundation issues — visible cracks, settling, or water intrusion

- Faulty mechanical systems — non-working HVAC, exposed wiring, outdated electrical panels without modern breakers

- Water damage or mold — visible staining, active leaks, compromised structural elements

- No hot water — water heater must be operational

- Bathroom not functional — toilet, sink, and shower must all work

- Inadequate drainage — standing water near foundation or in yard

- Missing or broken handrails — on stairs with four or more risers

- Crawl space issues — must be accessible, properly vented, and free of standing water

Practical advice: Get a standard home inspection before the FHA appraisal. A good inspector will catch most of these issues. If you know about a repair requirement ahead of time, you can negotiate for the seller to fix it or credit you for repairs — rather than being blindsided after an appraisal failure.

Manual Underwriting — Your Second Chance

If automated underwriting (AUS) returns a “Refer” instead of an “Approve,” that’s not always the end. FHA allows manual underwriting — where a human underwriter reviews your full file and makes a judgment call.

Manual underwriting is most often used for:

- Borrowers with credit scores below 580

- Non-traditional credit profiles (no credit score — but with rental and utility payment history)

- Recent bankruptcy or foreclosure with documented extenuating circumstances

- High DTI ratios with strong compensating factors

Under manual underwriting, the maximum DTI ratios are stricter: typically 31%/43% without compensating factors, but lenders have flexibility with documented compensating factors.

Not every FHA lender offers manual underwriting. This is a key reason to shop lenders — especially if you have a thin credit file, recent derogatory marks, or non-standard income.

What Happens If You’re Denied for an FHA Loan?

Getting denied isn’t the end. Here’s the action plan:

- Get the denial reason in writing

Lenders are required under the Equal Credit Opportunity Act (ECOA) to provide an Adverse Action Notice explaining why you were denied. - Identify which factor failed

- Credit score too low: dispute errors, pay down revolving balances (utilization below 30%), add an authorized user to a seasoned account with good history

- DTI too high: pay off small debt accounts, avoid taking new credit, consider a co-borrower

- Income documentation: work with a CPA to ensure your returns accurately reflect your income

- Property condition: find a different property or pursue a 203(k) loan

- Don’t apply at five lenders simultaneously

Multiple hard inquiries in a short window hurt your score. Within 45 days, all mortgage inquiries count as one for scoring purposes — but spread out applications strategically. - Apply with a different lender

One lender’s denial doesn’t disqualify you from FHA. Overlays vary significantly. A lender specializing in FHA with manual underwriting may approve what a retail bank rejected. - Wait and rebuild

If the issue is timing (too recent a bankruptcy, insufficient employment history), the 12–24 month window to rebuild is worth it. Use a secured credit card, make on-time payments, and keep utilization low.

Student Loan Calculation — A Hidden Trap Many Borrowers Miss

FHA updated its student loan guidelines in 2021 and they’re still commonly misapplied in 2026.

Current FHA rule (per HUD Handbook 4000.1): If monthly student loan payments are on your credit report, use that payment amount. If the loans are in deferment or forbearance, lenders must use 1% of the outstanding balance as the assumed monthly payment — not the actual deferred payment of $0.

Example: $75,000 in student loans in deferment. FHA treats this as $750/month in your DTI calculation — even though you’re paying nothing right now. This is a significant DTI impact that surprises many borrowers.

Workaround: If you’re on an income-driven repayment (IDR) plan with a documented payment, FHA allows using that actual payment amount — even if it’s $150/month on $75,000 in debt. Getting into an IDR plan before applying can meaningfully reduce your calculated DTI.

Real-World FHA Loan Case Study — Phoenix, Arizona, 2026

The borrower: Maria, 29, elementary school teacher

Income: $58,000/year ($4,833/month gross)

Credit score: 612

Savings: $14,000

Monthly debts: $310 car payment, $95 credit card minimums

Target home: $310,000 townhome in Phoenix suburbs

FHA loan math:

| Item | Amount |

| Purchase price | $310,000 |

| Down payment (3.5%) | $10,850 |

| Base loan amount | $299,150 |

| Upfront MIP (1.75%, rolled in) | $5,236 |

| Total loan amount | $304,386 |

| Interest rate | 6.35% (30-year fixed) |

| Monthly P&I | $1,901 |

| Monthly MIP (0.55%) | $140 |

| Estimated taxes + insurance | $350 |

| Total monthly payment | ~$2,391 |

DTI calculation:

Front-end: $2,391 / $4,833 = 49.5% — over standard limit

Resolution: Maria’s lender approved via manual underwriting. Compensating factors: stable 4-year employment with the same school district, 3 months of reserves post-closing, and zero payment shock (she was paying $1,800/month in rent).

Maria’s exit strategy: Refinance into conventional when her home reaches 20% equity. At current appreciation rates in Phoenix (roughly 4–5% annually), she projects hitting that milestone within 6–7 years. At that point, she eliminates $140/month in MIP and potentially gets a lower rate.

What Maria said (paraphrased from a client review shared publicly): “Every conventional lender told me to wait two more years. The FHA loan didn’t just get me approved — it got me into a home I already own while interest rates were manageable.”

Is an FHA Loan Right for You? — Decision Framework

Use this framework, not generic advice:

You should strongly consider FHA if:

- Credit score below 680

- Less than 10% saved for down payment

- Carrying student loans in deferment (DTI impact manageable)

- Need to use gift funds for entire down payment

- Self-employed with recent income growth (FHA manual underwriting more forgiving)

- Want to move in the next 6–12 months and can’t wait to save more

You should consider conventional instead if:

- Credit score 700 or above

- Can put down 20% (eliminates PMI entirely)

- Buying a condo in a non-FHA-approved building

- Want an investment property or vacation home

- Targeting a home with known repair issues that won’t pass FHA appraisal

- Your target market is extremely competitive and sellers prefer conventional buyers

You should skip FHA and look at VA if:

- You’re a veteran, active-duty service member, or surviving spouse

- VA loan = zero down, no mortgage insurance, better rates, no loan limit restrictions

You should look at USDA if:

- Buying in a designated rural or suburban area

- Income is below the USDA limit for your county

- USDA = zero down, lower fees than FHA, strict geographic restrictions

Frequently Asked Questions

What is an FHA loan and how does it work?

An FHA loan is a government-insured mortgage where the Federal Housing Administration guarantees private lenders against borrower default, allowing them to approve borrowers with lower credit scores and smaller down payments.

What credit score do I need for an FHA loan in 2026?

The FHA minimum is 580 for 3.5% down, or 500 for 10% down. However, most lenders impose a 600–620 minimum overlay — shop multiple lenders to find the best fit for your score.

Can I get an FHA loan with bad credit?

You can qualify with scores as low as 500 (with 10% down), and lenders offering manual underwriting may work with thin or imperfect credit files that automated systems reject.

How much is the FHA down payment?

Minimum 3.5% with a 580+ credit score. On a $300,000 home, that’s $10,500 — and it can come from savings, gift funds, or down payment assistance.

Can I remove FHA mortgage insurance?

For most borrowers, the only way to eliminate MIP is to refinance into a conventional loan once you have 20% equity. If you made a 10%+ down payment, MIP drops off after 11 years.

Are FHA loans only for first-time buyers?

No. FHA loans are available to any eligible borrower — first-time and repeat buyers alike. You just can’t have more than one FHA loan active at once (with narrow exceptions).

What are the FHA loan limits for 2026?

Standard areas: $541,287 for a single-family home. High-cost areas: up to $1,249,125. Multi-unit properties have higher limits.

How long does FHA loan approval take?

Typically 30–45 days from complete application to closing. Manual underwriting, appraisal issues, or slow documentation can extend this.

Can the seller pay my closing costs on an FHA loan?

Yes — the FHA allows seller concessions of up to 6% of the purchase price toward closing costs. Whether sellers agree depends on market conditions.

What is manual underwriting for FHA loans?

Manual underwriting is a human review of your full loan file when automated systems return a “Refer.” It allows for judgment-based approval for borrowers with complex financial profiles.

Can I use an FHA loan for a condo?

Yes, but the entire condo project must be FHA-approved. Check HUD’s condo database before making an offer. Non-approved projects require a separate Single Unit Approval process.

What happens if the FHA appraisal is lower than the purchase price?

You can renegotiate the price, pay the gap in cash, or walk away. The FHA loan amount cannot exceed the appraised value.

Conclusion — Your Next Step, Not a Summary

Here’s the honest version: FHA loans are a tool. Not a reward, not a guarantee, and not always the best option.

If your credit score is under 680 and you have less than 10% saved: FHA is almost certainly your fastest path to homeownership. Don’t wait two years trying to perfect your finances while prices outrun your savings rate.

If your score is 680–700 and you can put down 10%: Run the numbers on both FHA and conventional. At that credit range, the difference in conventional PMI vs. FHA MIP may favor FHA in the short term — but conventional’s cancelable PMI wins long-term.

If your score is above 700 and you can hit 20% down: Skip FHA. The lifetime MIP costs you more than it gives you back.

If MIP is pushing your monthly payment too high to afford the home you want: Adjust the purchase price, not the loan type. A $30,000 reduction in purchase price saves more per month than switching loan programs in most scenarios.

The one thing that matters most right now: Get pre-approved before you make a single offer. Not pre-qualified. Pre-approved — with actual underwriting. In 2026’s market, the difference between a pre-qualification letter and a fully underwritten approval is often the difference between getting the home or losing it to another buyer.

Talk to two or three FHA-approved lenders. Ask each one directly: “What are your credit score overlays? Do you offer manual underwriting? What’s your average time to close?” The answers will tell you who actually specializes in FHA lending and who just offers it as a side product.

The Federal Housing Administration was built to help real people buy real homes. It still does exactly that — if you go in with your eyes open.

About Author

Author: Javeed Dhillon is a mortgage and personal finance writer specializing in government-backed lending programs, first-time homebuyer education, and housing market analysis. His work is grounded in primary HUD documentation, HMDA data, and real borrower case studies.