Introduction

Home loans are a way to buy a house. They help people own homes and build long term wealth. Home loans can be complex. They do not have to be. This guide will help you understand home loans in a way.

This guide is designed to be easy to read and understand. It covers the basics of home loans including the types of loans how to apply and how to save money. We want to help you make choices when it comes to your home loan

1.what is home loan?

Basic Definition

Home loan is the loan you use to buy a house. The bank or lender holds the home as security until you repay the loan.

Key Elements

- The amount you borrow is called the principal.

- The interest is the cost of borrowing money.

- Tenure is how long you have to repay the loan. This is usually 15 to 30 years

- . Your monthly payment includes principal, interest, taxes and insurance.

Why mortgages matter

- Home loan helps you buy a home without paying all the money upfront.

- They give you profits, which means you can use the money to invest in things.

- You may also get tax advantages, which means you can save money on your taxes.

-

Types of Home Loans

Fixed Rate Mortgage

The fixed-rate mortgage is one where the interest rate is constant during the entire duration of the mortgage contract. This is important in that your monthly payments will be consistent throughout.

Benefits

- Your payment will always remain the same so you can plan your budget.

- You do not have to worry about your interest rate going up.

- You have long-term security, which means you know how much you will pay each month.

Drawbacks

- The interest rate may be higher than types of loans.

- If interest rates go down you may be stuck with a rate

Adjustable-rate mortgage

- An adjustable rate mortgage starts at a fixed interest rate but it can change over time.

Benefits

- Your monthly payments may be lower at first

- . This type of loan can be good if you only plan to own the house for a time.

Risks

- Your interest rate may go up over time which means your monthly payments may increase.

- You may not be able to predict what your payments will be each month.

FHA Loans

FHA loans are government-backed loans designed for income or first-time buyers.

📊 Table 1: Comparison of Major Home Loan Types |

|||||||||||||||||||||||||||||||||||

|

Features

- Down payment, often 3.5%

- Flexible loan requirements

Limitations

- Mortgage insurance required

- Loan limits apply

VA Loans

- VA loans are available to service members and veterans.

Benefits

- No down payment

- No mortgage insurance

- Competitive rates

USDA Loans

- USDA loans are designed for suburban buyers and rural.

Highlights

- Zero down payment and Income restrictions apply.

Jumbo Loans

- Used for high-value properties exceeding limits.

Considerations

- Higher credit requirements

- Larger down payments

3.Mortgage Interest Rates

How Rates Work

Interest rates determine how much you pay over time. Even small differences significantly impact the cost.

Factors Affecting Rates

Credit score:

a higher score lowers rates

Loan term: shorter terms are often cheaper

Market conditions: inflation,

Federal Reserve policies

Down payment: larger payments reduce risk

Fixed vs Variable Rates

- rates: stable and predictable

- Variable rates: fluctuate, with a balance of risk and reward

4.Loan Terms and Structures

Common Loan Terms

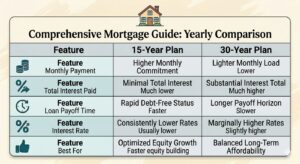

- 30-year loans: monthly payments, higher total interest

- Higher Payments for 15-year Mortgages = Lower Interest Costs

Amortization Explained

Amortization Defined

Payments are spread out over time with amortization.

Early payments have more interest and late payments have more principal..

-

Down Payments

- Standard Requirements

- Mortgages: 5% to 20%

- FHA Loans: As little as 3.5%

- VA and USDA Loans: Zero Percent

Advantages of a Larger Down Payment

- Lower monthly payments

- Reduced interest costs

- Avoid private mortgage insurance

-

Credit Score Importance

Score Ranges

- Excellent: 740+

- Good: 670-739

- Fair: 580-669

- Poor: Below 5

Impact on Mortgage

- Determines eligibility

- Affects interest rate

- Influences loan term

Improvement Tips

- Pay bills on time

- Reduce debt

- Avoid credit inquiries

-

Debt-to-Income Ratio (DTI)

Definition

DTI compares debt payments to income

.

Lenders use it to assess repayment ability

Ideal Ratios

- Below 36%: optimal

- Up to 43%: acceptable for loans

8.Pre-Approval Proces

What Is Pre-Approval?

A lender evaluates your profile and provides a conditional loan offer

Benefits

- Clarifies budget

- Strengthens offers

- Speeds up closing

Required Document

- Income statements, pay stubs, tax returns

- Credit history

- Bank statements

9.The Mortgage Application Process

Step-by-Step Overview

- Pre-approval: review

- Home search: property selection

- Loan application: submission

- Underwriting: risk assessment

- Closing: final agreement

-

Closing Costs

What Are Closing Costs?

Fees are paid at finalization

2% to 5% of the loan value

Common Fees

- Loan origination

- Appraisal

- Title insurance

- Legal fees

Cost Reduction Strategies

- Compare lenders

- Negotiate fees

- Request seller contributions

-

Private Mortgage Insurance (PMI)

When PMI Applies

PMI is required when the down payment is than 20% on conventional loans

Key Points

- Adds to cost

- Can be removed once equity reaches 20%

12. Refinancing Options

What Is Refinancing?

Refinancing replaces an existing mortgage with an one usually to improve terms.

Reasons to Refinance

* interest rates

* Shorten loan term

* Access home equity

Types of Refinancing

*Rate-and-term refinance

*Cash-out refinance

13.Home Equity and Its Use

Definition

Equity is the difference between property value and loan balance.

Uses

* Home improvements

*Debt consolidation

* Emergency funds

Common Mortgage Mistakes

Frequent Errors

* Overborrowing

* Ignoring loan cost

* Skipping pre-approval

* Not comparing lender

How to Avoid Them

* Plan budget carefully

* Understand terms fully

*Seek advice

-

Tips for First-Time Buyers

Practical Advice

* Start saving early

* Improve credit score

* Research loan options

* Get pre-

Smart Buying Strategies

*choose affordable homes

*Consider long-term needs

*Avoid emotional decisions

16.Current Trends in U.S. Mortgage Marke

Rising Interest Rates

Higher rates impact affordability

. Require strategic planning.

Digital Mortgage Platforms

online applications

, faster approvals and improved accessibility.

Flexible Loan Options

lenders offer tailored solutions catering to diverse borrowers.

-

Choosing the Right Lender

Factors to Consider

*Interest rates

* Fees and

closing costs

* Customer service

* Loan flexibility

Comparison Tips

* Request quotes

*Analyze total loan cost, not monthly payment

* Check reviews and ratings

18. Long-Term Financial Planning

Budgeting for Ownership

*Maintenance costs

*Property taxes

* Loan flexibility

* Insurance

Building Wealth Through Estate

* Appreciation over time

* Rental income potential

* Equity growth

-

Advantages of Homeownership

Key Benefits

* Stability: no rent increases

*Investment growth

*Tax deductions

Final Thoughts

When used and managed well, home loans can be a tool for building long-term wealth and, ultimately financial security. By learning the basics of comparing options and making plans, borrowers can jump-start decisions that will benefit them for decades.

Diving into this guide grants you a systematic and helpful foundation to positively, clearly, and successfully work through the process of home loans.