By Javeed Dhillon | Mortgage Research Specialist | Updated: May 2026 Verified against official VA.gov guidelines | YMYL-compliant | VA Loans (Veterans Affairs)

What is a VA loan?

A VA loan is a government-backed mortgage guaranteed by the Department of Veterans Affairs for eligible veterans, active-duty service members, National Guard and Reserve members, and certain surviving spouses. VA loans offer zero down payment, no private mortgage insurance (PMI), competitive interest rates, and flexible credit requirements — making them the most powerful home financing benefit earned through military service.

Official source: VA.gov Home Loans | Consumer protection info: CFPB Mortgages

Table of Contents

- What Is a VA Loan?

- VA Loan Benefits 2026

- VA Loan Eligibility Requirements

- Certificate of Eligibility (COE)

- VA Loan Types

- VA Funding Fee Rates (2026)

- Funding Fee Exemptions

- Credit Score & Income Requirements

- VA Loan Limits 2026

- VA Loan Closing Costs

- How to Apply — Step-by-Step

- VA vs. Conventional vs. FHA

- Common Myths — Debunked

- Real 2026 Example

- FAQs

What Is a VA Loan?

A VA loan is a mortgage backed by the U.S. Department of Veterans Affairs that lets eligible borrowers buy a home with zero down payment, no PMI, and lower-than-average interest rates.

The VA doesn’t lend money directly. Private lenders — banks, credit unions, and mortgage companies — issue the loan. The VA guarantees a portion of it, reducing lender risk. That guarantee is why veterans get terms no civilian mortgage can match.

The program launched in 1944 under the original GI Bill of Rights. Since then, the VA has guaranteed more than 28.5 million loans. In fiscal year 2025 alone, it backed 323,835 VA purchase loans — an 8.5% increase over 2024, showing the program is growing as more veterans learn what they’ve earned.

VA Loan Benefits 2026

VA loans offer five core advantages that no other mortgage product combines.

| Benefit | VA Loan | Conventional | FHA |

| Down Payment | $0 required | 3%–20% | 3.5% minimum |

| PMI / Mortgage Insurance | None | Required under 20% equity | Required (often life of loan) |

| Interest Rate | 0.25%–0.50% below market avg. | Market rate | Slightly above market |

| Loan Limit (Full Entitlement) | No limit | County-based | FHA limits apply |

| Upfront Insurance Cost | One-time funding fee (waivable) | None | 1.75% upfront MIP |

| Credit Score Floor | ~620 (lender overlay) | 620–740 | 580 |

-

Zero Down Payment

You can finance 100% of the purchase price with full entitlement. On a $400,000 home, that means keeping $40,000–$80,000 in your pocket instead of handing it to a lender as a down payment.

-

No Monthly PMI

Conventional loans require PMI below 20% equity. FHA loans charge mortgage insurance for the life of the loan in most cases. VA loans charge neither. On a $350,000 loan, eliminating PMI saves $150–$250 every month — up to $3,000/year.

-

Competitive Interest Rates

The VA guaranty lets lenders offer rates that consistently run 0.25%–0.50% below conventional averages in 2026. Over a 30-year loan, that difference is tens of thousands of dollars.

-

Reusable Benefit

VA loan entitlement is not a one-time use. Sell the home, pay off the VA loan, restore your entitlement — and the full benefit is available again for your next purchase.

-

Flexible Credit and Underwriting

The VA uses a residual income standard (cash left after all monthly expenses) alongside DTI ratios. This protects veterans from overextending and also allows approval in situations where conventional underwriting would say no.

VA Loan Eligibility Requirements

You qualify for a VA loan based on your service category, length of service, and discharge status.

Active-Duty Service Members

Eligible after 90 consecutive days of active service. A statement of service from your commanding officer confirms eligibility.

Veterans — Service Length by Era

| Service Period | Required Active Duty |

| Wartime | 90 days |

| Peacetime | 181 days continuous |

| Post-Sept. 7, 1980 (enlisted) | 24 months continuous OR full ordered period |

| Post-Oct. 16, 1981 (officers) | 24 months continuous OR full ordered period |

National Guard and Reserve Members

Eligible with any of the following:

- 6 years in the Selected Reserve or National Guard

- 90 days of active-duty service under Title 10 wartime orders

- Activation under qualifying Title 32 orders

Surviving Spouses

Eligible if the veteran spouse:

- Died in service or from a service-connected disability

- Is listed as MIA or POW

- Received a totally disabling service-connected disability before death (even if cause of death was unrelated)

The surviving spouse must not have remarried before age 57.

Discharge Status

Your discharge must be other than dishonorable. Honorable and general discharges qualify. If your discharge is classified otherwise, a discharge upgrade application through the VA Board for Correction of Military Records may restore eligibility.

Official eligibility tool: VA Eligibility Check — VA.gov

Certificate of Eligibility

A Certificate of Eligibility (COE) is the document your lender needs to confirm you qualify for a VA loan. Getting one takes minutes in most cases.

Three Ways to Get Your COE

- Through your lender — Most VA-approved lenders pull COEs electronically through the VA’s ACE system in minutes. This is the fastest method and requires no action from you.

- Online at VA.gov — Log in through DS Logon, My HealtheVet, or ID.me and request it directly.

- By mail — Submit VA Form 26-1880 with your DD-214 (veterans) or statement of service (active duty).

Your COE also shows your entitlement amount — the portion of the loan the VA guarantees. Full entitlement borrowers face no loan limits in 2026.

VA Loan Types

There are five VA-backed loan products in 2026. The right one depends on your goal.

VA Purchase Loan

Used to buy a primary residence. Eligible property types:

- Single-family homes

- VA-approved condominiums

- Manufactured homes on permanent foundations

- Multi-unit properties (up to 4 units, borrower must occupy one)

Properties must meet the VA’s Minimum Property Requirements (MPRs) — standards ensuring the home is safe, structurally sound, and sanitary.

VA IRRRL (Streamline Refinance)

The VA Interest Rate Reduction Refinance Loan lowers your rate on an existing VA loan with minimal paperwork. Key features:

- Funding fee: only 0.5% (lowest of any VA loan)

- No appraisal required in most cases

- No income verification in most cases

- Must result in a lower monthly payment (with exceptions for ARM-to-fixed conversions)

VA Cash-Out Refinance

Refinances any existing mortgage (VA or conventional) into a new VA loan and lets you pull equity as cash. Available for home improvements, debt payoff, or any purpose. Funding fee is the same as a purchase loan.

Native American Direct Loan (NADL)

VA-direct financing for eligible Native American veterans purchasing homes on Federal Trust land. The VA is the actual lender in this case.

Adapted Housing Grants

For veterans with qualifying service-connected disabilities:

| Grant | 2026 Maximum |

| Specially Adapted Housing (SAH) | $117,014 |

| Special Housing Adaptation (SHA) | $23,444 |

| Temporary Residence Adaptation (TRA) — SAH-eligible | $50,961 |

| Temporary Residence Adaptation (TRA) — SHA-eligible | $9,100 |

Source: VA Adapted Housing Grants — VA.gov

VA Funding Fee Rates (2026)

The VA funding fee is a one-time charge at closing that sustains the loan program. It ranges from 0.5% to 3.3% depending on loan type, down payment, and usage.

The fee replaced monthly mortgage insurance. Pay it once at closing — or roll it into the loan — and you’re done. No recurring premiums.

Purchase Loan Funding Fee — 2026

| Down Payment | First-Time Use | Subsequent Use |

| Less than 5% | 2.15% | 3.30% |

| 5%–9.99% | 1.50% | 1.50% |

| 10% or more | 1.25% | 1.25% |

Refinance Loan Funding Fee — 2026

| Loan Type | Fee |

| IRRRL (Streamline Refinance) | 0.50% |

| Cash-Out Refinance — First Use | 2.15% |

| Cash-Out Refinance — Subsequent Use | 3.30% |

Source: VA Funding Fee — VA.gov

How the Funding Fee Is Paid

- Finance it — Roll it into the loan balance. Most borrowers choose this. It adds to your loan amount and monthly payment but requires no cash at closing.

- Pay at closing — Pay cash upfront. Reduces your loan balance and long-term interest. Best if you have reserves to spare.

2026 Tax Deduction (New)

Starting tax year 2026, the VA funding fee is tax deductible for eligible borrowers who itemize deductions on Schedule A (Form 1040). This does not affect cash-to-close or your mortgage approval. Consult a qualified tax professional to claim it correctly.

Source: CFPB — Mortgage Closing Costs

Funding Fee Exemptions

If you qualify for an exemption, you pay zero funding fee — saving $4,000–$10,000+ on a typical purchase.

You are exempt if you are:

- Receiving VA compensation for any service-connected disability (10% rating or higher)

- Eligible for disability compensation but receiving military retirement or active-duty pay instead

- A Purple Heart recipient serving on active duty at closing

- An eligible surviving spouse receiving Dependency and Indemnity Compensation (DIC)

Approximately 6 million of the 18 million U.S. veterans receive disability compensation — meaning they qualify for a complete funding fee waiver.

Action step: Check your disability status before locking a rate. If you have an open disability claim, the exemption can be applied retroactively. Confirm exemption status on your COE and have your lender verify it on the Closing Disclosure before closing day.

Credit Score and Income Requirements

Credit Score

Most VA lenders in 2026 require a minimum 620–640 credit score. The VA itself sets no official minimum. Some lenders approve lower scores with strong compensating factors:

- High residual income

- Low debt-to-income ratio

- Significant cash reserves

- Long, stable employment history

Reference: FHFA Credit Score Standards

Debt-to-Income (DTI) Ratio

The VA prefers DTI at or below 41%, but this is a guideline, not a hard cap. Strong residual income can allow for higher DTI on a case-by-case basis.

Residual Income — The VA’s Unique Standard

Residual income is the money remaining after paying all major monthly obligations. It’s the most veteran-friendly feature of VA underwriting — it measures real ability to sustain homeownership.

Residual income requirements by region and family size (sample):

| Region | Family of 1 | Family of 4 |

| Northeast | $450/month | $1,025/month |

| Midwest | $441/month | $1,003/month |

| South | $441/month | $1,003/month |

| West | $491/month | $1,117/month |

Source: VA Lenders Handbook — VA.gov

Employment and Income Documentation

Lenders typically require:

- Minimum 2 years of stable employment history

- W-2s, tax returns, and 30 days of recent pay stubs

- Self-employed veterans need 2 years of tax returns plus a year-to-date profit/loss statement

VA Loan Limits 2026

Borrowers with full VA entitlement have no loan limits in 2026. You can borrow as much as a lender will approve based on your income and the appraised value of the property.

Loan limits only apply to borrowers with partial entitlement — meaning they have an existing active VA loan or previously defaulted on a VA loan without repaying it in full.

For partial entitlement borrowers, county loan limits are tied to FHFA conforming loan limits:

| Limit Type | 2026 Amount |

| Baseline conforming loan limit | $832,750 |

| High-cost area maximum (varies by county) | Up to $1,209,750 |

Source: FHFA 2026 Conforming Loan Limits

With partial entitlement, you can still borrow above the limit — but you’ll need a down payment equal to 25% of the amount exceeding your remaining guaranty.

VA Loan Closing Costs

VA loans don’t eliminate closing costs, but they cap what lenders can charge and prohibit certain fees entirely.

The 1% Origination Fee Rule

Lenders may charge up to 1% of the loan amount as a flat origination fee. They cannot stack itemized processing, underwriting, or overhead fees on top of this 1% cap.

Typical VA Loan Closing Costs

| Cost Item | Typical Range | Who Pays |

| VA Funding Fee | 0.5%–3.3% of loan | Buyer (or financed) |

| VA Appraisal | $500–$800 | Buyer |

| Lender Origination Fee | Up to 1% of loan | Buyer |

| Title Insurance & Settlement | $800–$1,500 | Negotiable |

| Credit Report | $30–$50 | Buyer |

| Recording Fees | $100–$300 | Buyer |

| Prepaid Interest, Taxes & Insurance | Varies | Buyer |

| Discount Points (optional) | Per point = 1% of loan | Buyer |

Fees VA Prohibits Lenders from Charging

- Attorney fees for the lender’s benefit

- Broker fees

- Prepayment penalties

- Loan closing or settlement fees charged by the lender

- Escrow amounts prohibited by VA guidelines

Seller Concessions

Sellers can pay up to 4% of the home’s reasonable VA-appraised value toward permitted concessions — including the funding fee, prepaid items, and other VA-allowed costs. Standard closing costs are paid separately outside this 4% cap.

In a buyers’ market, negotiating seller concessions can bring your cash to close to near zero.

Reference: HUD Settlement Costs Guide

How to Apply

Applying for a VA home loan takes 8 steps. Most veterans close in 21–30 days with a prepared file and an experienced lender.

Step 1 — Confirm Eligibility

Review the service requirements above. If you served and received an honorable or general discharge, you very likely qualify. Start at VA.gov eligibility.

Step 2 — Obtain Your Certificate of Eligibility (COE)

Your VA-approved lender can pull this electronically in minutes. Have your DD-214 (veterans) or statement of service (active duty) ready.

Step 3 — Choose a VA-Experienced Lender

Not all lenders are equal on VA loans. A lender who closes VA files weekly understands VA appraisals, MPRs, and underwriting — and won’t add unnecessary overlays to VA guidelines. Shop at least 3 lenders and compare Loan Estimates.

Step 4 — Get Pre-Approved

Submit income documents, bank statements, and employment history. The lender checks credit, calculates DTI and residual income, and issues a pre-approval letter showing your verified purchasing power.

Step 5 — Find Your Home

Work with a buyer’s agent experienced in VA transactions. The property must be your primary residence and meet VA Minimum Property Requirements.

Step 6 — VA Appraisal

The lender orders a VA appraisal by a VA-assigned appraiser. The appraisal confirms:

- The home’s market value

- That the property meets VA MPRs

The VA appraisal is not a home inspection. Always order a separate professional home inspection — it protects you, not the lender.

Step 7 — Underwriting

The lender’s underwriting team reviews your full file — income, credit, assets, appraisal, and COE. Respond to any requests for additional documentation quickly to avoid delays.

Step 8 — Close

Sign your loan documents. If you financed the funding fee, it’s already in the loan. Your cash at closing covers prepaids, escrow setup, and any remaining negotiated closing costs.

VA vs. Conventional vs. FHA

Which loan is right for you depends on your service status, credit, down payment, and how long you plan to stay in the home.

| Factor | VA Loan | Conventional | FHA |

| Who Can Use It | Veterans, service members, surviving spouses | Anyone | Anyone |

| Down Payment | $0 | 3%–20% | 3.5% |

| PMI/MIP | None | Required < 20% equity | Required (often for loan life) |

| Upfront Insurance | One-time funding fee (0.5%–3.3%) | None | 1.75% upfront MIP |

| Ongoing Insurance | None | PMI until 20% equity | Annual MIP (0.55%–1.05%/yr) |

| Interest Rate | Typically lowest | Market | Slightly above market |

| Best For | Eligible veterans, especially low-cash buyers | High-equity, excellent-credit buyers | Low-credit, lower-income buyers |

When Conventional Might Win

If you have a 760+ credit score, 20% down, and no need to finance a funding fee — a conventional loan with zero PMI and zero upfront costs may be competitive. Always run both scenarios with a VA-experienced lender before deciding.

Common Myths — Debunked

Myth: “VA loans are slower to close.” False. With an experienced VA lender, closing timelines match conventional loans — typically 21–30 days. Delays are lender-related, not VA-related.

Myth: “You only get one VA loan.” False. Entitlement is reusable. Sell the home, pay off the loan, restore entitlement — you can use the benefit again and again.

Myth: “Sellers won’t accept VA offers.” Largely outdated. In most 2026 markets, a clean VA pre-approval competes fine. The VA appraisal is the only real variable, and experienced agents handle it routinely.

Myth: “You need perfect credit.” False. VA underwriting uses residual income alongside credit score. Borrowers approved with 620 credit scores and strong residual income regularly close VA loans that conventional programs would reject.

Myth: “VA loans can be used for investment properties.” False. VA loans require owner-occupancy — you must intend to move in as your primary residence within 60 days of closing. You can buy a multi-unit property (up to 4 units) and rent the other units while you live in one.

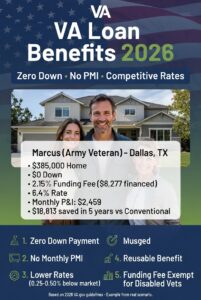

Real 2026 Example

A complete financial picture showing what a VA loan actually costs — and saves — in 2026.

Borrower: Marcus, Army veteran, first-time VA loan user, buying in Dallas, TX Purchase Price: $385,000 Down Payment: $0 (full entitlement) Funding Fee: 2.15% = $8,277 (financed into loan) Total Loan Amount: $393,277 Interest Rate: 6.4% (30-year fixed VA loan) Monthly Principal & Interest: ~$2,459 Monthly PMI: $0

Comparison: Same Purchase, Conventional Loan (3% down)

| Cost Item | VA Loan | Conventional (3% down) |

| Down Payment | $0 | $11,550 |

| Upfront Mortgage Insurance | $8,277 (funded into loan) | $0 |

| Monthly PMI | $0 | ~$185/month |

| PMI Total (7 years to 20% equity) | $0 | $15,540 |

| Cash Needed at Closing | ~$3,000 (prepaids/escrow) | ~$14,550+ |

5-Year Savings with VA Loan: ~$18,813 — mostly from eliminated PMI and preserved down payment cash.

Marcus’s funding fee ($8,277) is offset within 3.8 years through PMI savings alone. After that, every month is pure savings.

FAQs

What is a VA loan, and who offers them?

A VA loan is a government-backed mortgage guaranteed by the Department of Veterans Affairs and issued by VA-approved private lenders — banks, credit unions, and mortgage companies.

Can I use a VA loan more than once?

Yes. VA entitlement restores after you sell the home and pay off the VA loan, letting you reuse the benefit for future purchases.

What credit score do I need for a VA loan in 2026?

Most VA lenders require a minimum 620–640. The VA itself sets no official minimum credit score.

Is there a VA loan limit in 2026?

No limit for borrowers with full entitlement. Partial entitlement borrowers face county-based limits tied to the $832,750 conforming baseline.

What is the VA funding fee in 2026?

It ranges from 0.5% (IRRRL) to 3.3% (subsequent-use purchase, no down payment). First-time purchase with no down payment: 2.15%. Disabled veterans are fully exempt.

Is the VA funding fee tax deductible in 2026?

Yes — starting tax year 2026, it’s deductible for borrowers who itemize on Schedule A. Consult a tax professional. It does not affect your mortgage approval or closing costs.

Can I use a VA loan for an investment property?

No. VA loans require owner-occupancy as a primary residence. Multi-unit properties (up to 4 units) are allowed if you live in one unit.

How long does VA loan approval take?

With an experienced lender and a complete file, VA loans typically close in 21–30 days — the same as conventional loans.

Do I need a down payment?

No down payment is required for full entitlement borrowers. A down payment is optional and reduces your funding fee tier.

What are VA Minimum Property Requirements?

MPRs ensure the home is safe, structurally sound, and sanitary. They cover roofing, heating systems, plumbing, electrical, and structural integrity. Reviewed during the VA appraisal.

Can a surviving spouse use a VA home loan?

Yes. Eligible surviving spouses — those whose spouse died in service or from a service-connected disability, and who meet the VA’s remarriage rules — can use the VA home loan benefit.

What happens if the VA appraisal comes in low?

You can renegotiate the purchase price, pay the difference in cash, request a Reconsideration of Value with new comparable sales, or walk away using the VA escape clause and recover your earnest money.

Conclusion

The VA home loan is not just a mortgage — it’s one of the most significant financial benefits earned through military service. In 2026, it remains unmatched: zero down payment, no PMI, rates running 0.25%–0.50% below the conventional average, and no loan limits for full entitlement borrowers.

The one-time VA funding fee is the program’s trade-off, but it’s offset by PMI savings within 2–4 years for most borrowers — and waived entirely for the roughly 6 million veterans currently receiving disability compensation.

If you served, start here: check your eligibility, pull your COE, and compare at least three VA-approved lenders. The benefit is already yours. Using it correctly is what this guide is for.

For official information, eligibility decisions, and loan center contacts, visit VA.gov.

About the Author

Javeed Dhillon is a mortgage research specialist and financial writer with over a decade of experience covering veterans’ benefits, real estate financing, and personal finance. His work focuses on translating complex government loan programs into plain-language guidance that helps veterans make informed decisions. Javeed’s research draws exclusively on primary sources — VA.gov, CFPB, FHFA, and HUD — to ensure accuracy in a YMYL content category where outdated or incorrect information causes real financial harm.