Project Financing: The Complete Guide to Funding Large-Scale Projects in 2026

By Javeed Dhillon | Updated: May 2026

“The difference between a dream project and a built project is almost always financing.” — A truth every infrastructure developer learns the hard way.

Introduction

Big infrastructure projects are rarely built using a company’s own money alone. Whether it’s a solar power plant, highway, airport, or transmission network, most large-scale developments rely on project financing — a structure where future project revenues are used to repay investors and lenders. In recent years, project finance has become one of the most important tools for funding energy, infrastructure, and industrial growth worldwide. This guide explains how project financing works, the key parties involved, common financing structures, major risks, and the trends shaping the market in 2026

Table of Contents

- What Is Project Financing?

- Project Financing vs. Corporate Financing

- Key Players in a Project Finance Transaction

- How Project Financing Works — Step by Step

- Types of Project Financing Structures

- Sources of Funding in Project Finance

- Risk Allocation in Project Finance

- The Special Purpose Vehicle (SPV) Explained

- Sectors That Use Project Finance Most

- Real-World Example: SunZia Wind Project (2026)

- Project Finance in 2026 — Trends and Outlook

- Advantages and Disadvantages of Project Financing

- Key Financial Metrics and Ratios

- How to Prepare a Bankable Project Finance Proposal

- FAQs on Project Financing

- Conclusion

What Is Project Financing?

Project financing is a method of funding a long-term capital project through a stand-alone legal entity — typically a Special Purpose Vehicle (SPV) — where lenders look primarily at the project’s future cash flows as the basis for loan repayment, rather than the creditworthiness or assets of the project sponsors.

In simpler terms: the project pays for itself.

This is not a conventional business loan. There is no personal guarantee from a CEO or a mortgage on a corporate headquarters. If the project fails, lenders have recourse only to the project’s assets — its contracts, physical infrastructure, and revenue streams — not to the parent company’s broader holdings. This is why it’s called non-recourse or limited-recourse financing.

Core Definition (Featured Snippet Ready)

Project financing is the structured, long-term financing of a specific infrastructure or industrial project through a Special Purpose Vehicle (SPV), where repayment depends entirely on the project’s projected cash flows and assets, rather than the balance sheet of the sponsoring companies.

This model is used in:

- Power generation and energy projects

- Roads, bridges, and toll infrastructure

- Pipelines and water treatment facilities

- Hospitals and schools (PPP projects)

- Mining and natural resource extraction

- Large-scale real estate development

-

Project Financing vs. Corporate Financing

Most businesses borrow money using corporate finance — banks lend based on the company’s credit history, existing assets, and balance sheet strength. Project finance is fundamentally different.

| Feature | Project Financing | Corporate Financing |

| Repayment Source | Project cash flows | Company’s general revenues |

| Recourse to Sponsor | None (or limited) | Full recourse |

| Legal Structure | SPV / standalone entity | Parent company directly |

| Balance Sheet Impact | Off-balance sheet | On-balance sheet |

| Typical Loan Tenor | 10–30 years | 1–10 years |

| Risk Allocation | Distributed across parties | Borne by borrower |

| Complexity | Very high | Moderate |

| Used For | Large infrastructure, energy | General business needs |

| Due Diligence | Extensive (12–18 months) | Moderate (weeks) |

The key advantage of project finance from a sponsor’s perspective is risk isolation. If a major energy company builds five power plants using project finance, and one plant fails, only that plant’s SPV goes into default — the other four plants and the parent company remain untouched.

-

Key Players in a Project Finance Transaction

A project finance deal is never a two-party negotiation. It typically involves a web of stakeholders, each with a defined role, rights, and obligations.

The Core Participants

- Project Sponsors These are the companies or entities that initiate and develop the project. They contribute equity capital and take on the role of project developer and manager. Sponsors can be:

- Industrial sponsors (energy companies, construction firms)

- Public sponsors (government bodies, municipalities)

- Contractor sponsors (EPC contractors taking equity)

- Financial sponsors (private equity, infrastructure funds)

-

Lenders / Debt Providers

- Commercial banks (senior debt)

- Development Finance Institutions (World Bank, IFC, ADB)

- Export credit agencies

- Institutional investors (via project bonds)

- Multilateral agencies

- Offtakers The entity that purchases the project’s output — electricity, water, gas, toll revenue — under a long-term agreement. Offtaker creditworthiness is critical to bankability.

- EPC Contractors Engineering, Procurement, and Construction contractors who build the project. They take on construction risk and are often bound by fixed-price, turnkey contracts.

- O&M Operators Operations and Maintenance service providers who run the project after construction, ensuring it meets performance standards.

- Government / Regulatory Bodies Provide permits, licenses, concessions, and sometimes direct financial support or guarantees.

- Financial Advisors and Legal Counsel Structure the deal, draft contracts, conduct due diligence, and coordinate between all parties.

- Insurance Providers Cover construction risk, political risk, force majeure, and other project-specific exposures.

-

How Project Financing Works — Step by Step

Understanding the lifecycle of a project finance transaction helps demystify why it takes so long — and why it works.

Phase 1: Project Identification and Feasibility

The sponsor identifies an opportunity. Technical studies, environmental impact assessments, and financial models are developed to assess viability. A preliminary cost-benefit analysis determines if economic benefits outweigh costs.

Phase 2: Structuring the Deal

- An SPV is incorporated as a standalone legal entity

- The debt-to-equity ratio is determined (typically 70:30 to 90:10)

- Risk allocation is negotiated across parties

- Offtake agreements, EPC contracts, and O&M agreements are drafted

Phase 3: Due Diligence

Lenders conduct exhaustive due diligence — technical, legal, financial, environmental. Independent advisors are appointed. This phase can take 6 to 18 months.

Phase 4: Financial Close

All financing agreements are signed, conditions precedent are satisfied, and funds become available. This is the milestone every project team works toward.

Phase 5: Construction

The EPC contractor builds the project. Funds are drawn down from the loan facility in tranches as milestones are reached.

Phase 6: Operations and Debt Repayment

Once the project reaches commercial operation, revenues flow in. The waterfall structure directs cash to: (1) operating costs, (2) debt service (principal + interest), (3) reserve accounts, (4) dividends to equity sponsors.

Phase 7: Project Completion and Refinancing

After the loan is repaid, sponsors may refinance, sell the asset, or continue operations as a cash-generating infrastructure asset.

-

Types of Project Financing Structures

Not all project finance looks the same. The structure depends on the risk profile, the sector, and who is taking on what exposure.

Non-Recourse Financing

The purest form of project finance. Lenders have no claim on sponsor assets beyond the SPV. If the project fails, lenders can only seize the project’s assets and contracts. This protects sponsors but demands extremely thorough risk mitigation before lenders agree.

Limited-Recourse Financing

The most common structure in practice. Sponsors provide some guarantees during the riskiest phases — typically the construction period — and recourse is reduced or eliminated once the project reaches operational status.

Build-Operate-Transfer (BOT)

A private company builds and operates the infrastructure for a defined concession period, generating revenue (e.g., tolls), then transfers ownership to the government. Common in highways, airports, and water utilities.

Build-Transfer-Operate (BTO)

The private company builds and immediately transfers ownership, then operates under a service concession agreement.

Public-Private Partnerships (PPP)

Government and private sector share investment, risk, and returns. Used extensively in social infrastructure (hospitals, schools) and transport. The government provides revenue certainty through availability payments or demand guarantees.

Mezzanine Financing

A hybrid between debt and equity — typically subordinated debt that converts to equity if the borrower defaults. Mezzanine fills the gap between senior debt and equity, accepting higher risk for higher returns.

Project Bonds

Instead of borrowing from banks, sponsors issue bonds in capital markets. Institutional investors (pension funds, insurance companies) purchase these bonds for stable, long-term yields. Popular in mature infrastructure markets.

-

Sources of Funding in Project Finance

| Funding Source | Type | Typical Share | Key Features |

| Commercial Banks | Senior Debt | 40–60% | Fixed or floating rate, secured |

| Development Finance Institutions | Senior/Subordinated Debt | 10–20% | Lower rates, longer tenors |

| Export Credit Agencies | Guaranteed Debt | 10–15% | Support cross-border projects |

| Project Bonds | Capital Markets Debt | 10–30% | Institutional investors |

| Equity (Sponsors) | Equity | 10–30% | Risk capital, last to be repaid |

| Mezzanine Funds | Hybrid | 5–15% | Higher yield, subordinated |

| Government Grants/Viability Gap Funding | Grant/Subsidy | Variable | Fills financial viability gaps |

| Green Bonds / ESG Finance | Debt | Growing | Tied to environmental criteria |

| Tax Equity | Tax Benefits | Variable | Common in US renewables (IRA credits) |

-

Risk Allocation in Project Finance

Risk management is the beating heart of project finance. The fundamental principle is: each risk should be borne by the party best equipped to manage it.

Key Risks and Who Bears Them

Construction Risk

- What: Cost overruns, delays, technical failure during build

- Who bears it: EPC contractor through fixed-price, date-certain contracts

- Mitigation: Performance bonds, liquidated damages clauses, completion guarantees

Market / Revenue Risk

- What: Demand falls short of projections; commodity prices collapse

- Who bears it: Offtaker (through Power Purchase Agreements, take-or-pay contracts)

- Mitigation: Long-term offtake agreements with creditworthy counterparties

Operating Risk

- What: Project underperforms or maintenance costs exceed projections

- Who bears it: O&M contractor under performance-based contracts

- Mitigation: Performance ratios, reserve accounts, step-in rights for lenders

Political and Regulatory Risk

- What: Government changes laws, expropriates assets, changes tariff structures

- Who bears it: Government (through concession agreements) and insurance

- Mitigation: Political risk insurance, investment treaties, government guarantees

Interest Rate and Currency Risk

- What: Floating rate debt increases cost; currency mismatch creates exposure

- Who bears it: Sponsor and lender (shared)

- Mitigation: Interest rate swaps, hedging instruments, local currency financing

Force Majeure Risk

- What: Natural disasters, pandemics, wars

- Who bears it: Allocated case by case

- Mitigation: Insurance, force majeure clauses, reserve accounts

-

The Special Purpose Vehicle (SPV) Explained

The Special Purpose Vehicle — also called a Special Purpose Entity (SPE) or Project Company — is the legal and financial backbone of every project finance transaction.

What Is an SPV?

An SPV is an independent legal entity created specifically to own and operate the project. It is entirely separate from the sponsor companies, meaning:

- Its assets and liabilities do not appear on the sponsors’ balance sheets (off-balance-sheet financing)

- If the SPV defaults, sponsors’ other assets are protected

- Lenders’ claims are “ring-fenced” within the SPV

SPV Structure Example

[Sponsor A] + [Sponsor B] + [Financial Investor]

↓ (Equity)

[SPV / Project Company]

↓ ↓

[EPC Contractor] [Senior Lenders]

(Construction) (Debt — 70-80%)

↓

[O&M Operator]

(Operations)

↓

[Offtaker] ← [Revenue/Cash Flows]

Why Lenders Accept SPV Risk

Lenders compensate for the lack of sponsor recourse through:

- Comprehensive contractual security — pledge over all project contracts and accounts

- Debt Service Reserve Accounts (DSRA) — typically 6 months of debt service held in escrow

- Cash flow waterfall — strict priority of payments protecting debt service

- Step-in rights — ability to take control of the project if performance deteriorates

- Covenant packages — financial ratios the SPV must maintain

-

Sectors That Use Project Finance Most

Project finance is concentrated in sectors with predictable long-term cash flows and high capital requirements.

Energy and Power

The largest sector by volume. Includes coal (declining), gas, nuclear, solar, wind, hydro, and energy storage. Power Purchase Agreements (PPAs) provide the revenue certainty lenders need.

Infrastructure

Roads, bridges, tunnels, airports, seaports, rail. Often structured as PPP or BOT concessions with government revenue guarantees.

Oil, Gas, and LNG

Upstream extraction, midstream pipelines, and LNG liquefaction terminals. Complex multi-decade projects with offtake backed by long-term supply contracts.

Mining

Large-scale mining projects — copper, gold, lithium, phosphate — use project finance, often with offtake secured to creditworthy commodity traders or processors.

Renewables and Clean Energy

The fastest-growing segment in 2026. Solar, wind, battery storage, green hydrogen, and renewable fuels all use project finance structures enhanced by ESG mandates, green bonds, and tax equity.

Telecommunications

Subsea cables, satellite infrastructure, and tower networks use project finance structures backed by capacity lease agreements.

Social Infrastructure

Hospitals, schools, and prisons through PPP frameworks where government availability payments replace market revenue risk.

-

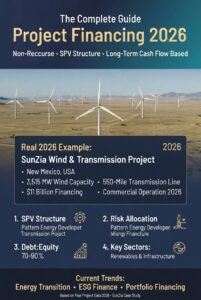

Real-World Example: The SunZia Wind and Transmission Project (2026)

One of the most instructive real-world examples of project financing in action is the SunZia Wind and Transmission Project in the United States.

Project Overview:

- Location: New Mexico, USA

- Capacity: 3,515 MW of wind generation

- Transmission: 550-mile, 525 kilovolt transmission line delivering power to Arizona and California

- Financing Secured: $11 billion (December 2023)

- Expected Commercial Operation: 2026

Why This Project Matters for Project Finance:

The SunZia project demonstrates every core feature of modern project finance:

- SPV Structure — The project was developed through a dedicated project company, isolating it from the broader balance sheet of Pattern Energy (the developer)

- Non-recourse debt — Lenders’ security was entirely based on projected power sales revenues, backed by long-term PPAs

- Risk allocation — Construction risk was allocated to the EPC contractors; market risk was managed through offtake agreements with California and Arizona utilities

- Government support — Federal permitting and grid interconnection agreements provided regulatory certainty

- ESG finance — Green bond and sustainable debt facilities were used given the project’s clean energy credentials

The SunZia deal is a benchmark for how large-scale renewable energy project finance works in 2026 — combining commercial bank debt, institutional capital markets funding, and tax equity in one integrated structure.

-

Project Finance in 2026 — Trends and Outlook

The project finance market in 2026 is being reshaped by several powerful forces:

-

Energy Transition Dominance

Renewables and energy storage have overtaken fossil fuels as the primary focus of project finance globally. The International Energy Agency projects that clean energy investment will surpass $2 trillion annually by 2026, with a significant share structured through project finance vehicles.

-

Tighter Lender Underwriting

Particularly in the energy storage sector, lenders are applying more rigorous due diligence around technology performance, degradation risk, and merchant revenue exposure. The era of easy money for any clean energy project is over — bankability now requires proven technology and contracted revenues.

-

Tax Equity and IRA Impact (US Market)

The US Inflation Reduction Act (IRA) continues to reshape the US project finance market. Investment Tax Credits (ITC) and Production Tax Credits (PTC) are being monetized through tax equity structures, bringing new investors — including major corporates — into renewable project financing.

-

Portfolio Financing

Rather than financing individual projects, sponsors are increasingly bundling multiple projects into portfolio financings to spread risk, reduce transaction costs, and achieve better terms. This trend is particularly prevalent in solar and onshore wind.

-

ESG and Green Finance Standards

Environmental, Social, and Governance (ESG) criteria are now embedded in most major lenders’ credit policies. Projects must demonstrate compliance with Equator Principles, IFC Performance Standards, and climate-aligned taxonomies to access financing from development banks and many commercial lenders.

-

Digital Infrastructure Financing

Data centers, subsea fiber cables, and satellite networks are emerging as significant new asset classes in project finance, driven by the AI and cloud computing boom.

-

Emerging Markets Growth

Africa, Southeast Asia, and Latin America are attracting increasing project finance flows, backed by Development Finance Institutions like the IFC, AfDB, and ADB, which are stepping in to mitigate political and regulatory risks that commercial banks avoid.

-

Advantages and Disadvantages of Project Financing

Advantages

For Sponsors:

- Off-balance-sheet treatment — keeps corporate debt ratios healthy

- Risk isolation — project failure doesn’t threaten the sponsor’s other businesses

- Leverage — access high debt ratios (70–90%) unavailable in corporate finance

- Access to large capital — enables projects too large for any single company’s balance sheet

- Structured risk sharing — contractual allocation of construction, operational, and market risk

For Lenders:

- Security package — comprehensive pledge over all project assets and contracts

- Cash flow visibility — long-term offtake agreements provide repayment certainty

- High-value relationships — project finance builds deep relationships with major sponsors

- Diversification — infrastructure loans have low correlation with corporate credit cycles

For Government/Society:

- Mobilizes private capital for public infrastructure without increasing public debt

- Risk transfer to private sector improves project execution discipline

- Technology and expertise transfer through private sector involvement

Disadvantages

Complexity and Cost:

- Extensive legal, technical, and financial due diligence drives high upfront transaction costs

- Negotiations can take 12–24 months before financial close

- Legal fees, advisor fees, and arrangement fees can total 2–5% of project value

Operational Constraints:

- Lenders impose restrictive covenants — limited ability to change project scope, take on new debt, or pay dividends until financial ratios are met

- Step-in rights mean lenders can effectively take control of the project if performance deteriorates

Refinancing Risk:

- If market conditions worsen during the construction phase, refinancing may be unavailable or prohibitively expensive

-

Key Financial Metrics and Ratios in Project Finance

Lenders and sponsors use several critical financial metrics to assess project viability and monitor performance.

| Metric | Definition | Typical Threshold |

| DSCR (Debt Service Coverage Ratio) | Annual cash flow available for debt service ÷ Annual debt service | Minimum 1.20–1.40x |

| LLCR (Loan Life Coverage Ratio) | NPV of cash flows over loan life ÷ Outstanding debt | Minimum 1.30–1.50x |

| PLCR (Project Life Coverage Ratio) | NPV of cash flows over project life ÷ Outstanding debt | Minimum 1.50–2.00x |

| IRR (Internal Rate of Return) | Return rate at which NPV = 0 | Varies by sector (8–15% equity IRR) |

| Debt-to-Equity Ratio | Total debt ÷ Total equity | Typically 70:30 to 80:20 |

| Gearing | Debt as % of total project cost | 65–85% in mature markets |

Understanding DSCR in Practice

The Debt Service Coverage Ratio (DSCR) is the single most important ratio in project finance. A DSCR of 1.25x means the project generates 25% more cash than needed to service its debt in any given period. Lenders set minimum DSCR covenants — if the ratio falls below the threshold, the project is in technical default even if no payment has been missed.

-

How to Prepare a Bankable Project Finance Proposal

Whether you’re approaching a commercial bank, a development finance institution, or a private infrastructure fund, a bankable project finance proposal needs to address these elements:

-

Executive Summary

- Project description, location, and scale

- Total project cost and financing structure sought

- Key sponsors and their track record

- Revenue model and offtake arrangements

-

Technical Feasibility Study

- Engineering design and technology assessment

- Construction timeline and EPC contractor qualifications

- Operations plan and performance projections

-

Financial Model

- 25–30 year cash flow projections

- Sensitivity analysis (base case, downside, stress scenarios)

- DSCR, LLCR, PLCR calculations under each scenario

- IRR for equity investors

-

Contractual Framework

- Offtake agreements (PPAs, take-or-pay, capacity payments)

- EPC contract summary (fixed price, completion guarantee)

- O&M agreement

- Land and resource agreements

-

Risk Matrix

- Comprehensive identification of all project risks

- Allocation of each risk to the appropriate party

- Mitigation measures for each risk

-

Environmental and Social Impact Assessment (ESIA)

- Compliance with Equator Principles, IFC standards, national regulations

- Stakeholder engagement plan

- Environmental management plan

-

Legal Structure

- SPV incorporation details

- Security package (pledge of assets, accounts, contracts)

- Governing law and dispute resolution

-

Sponsor Track Record

- Comparable projects developed and financed

- Management team credentials

- Financial statements of sponsor entities

-

Frequently Asked Questions (FAQs) About Project Financing

What is the difference between project finance and project funding?

Project finance refers specifically to the structured, non-recourse debt financing of a project through an SPV. Project funding is a broader term covering all sources of capital — debt, equity, grants, and subsidies — used to fund a project.

How long does project financing typically take?

From mandate to financial close, project finance transactions typically take between 12 and 24 months, depending on project complexity, jurisdiction, and market conditions.

What is a non-recourse loan in project finance?

A non-recourse loan is one where the lender’s only recourse in the event of default is the project’s own assets and cash flows — the lender cannot pursue the sponsor’s other assets or balance sheet.

What is an offtake agreement and why is it important?

An offtake agreement is a long-term contract to purchase the project’s output (electricity, gas, water, etc.) at agreed prices. It provides the revenue certainty that makes the project bankable and enables lenders to model predictable debt repayment.

What is a Debt Service Reserve Account (DSRA)?

A DSRA is a cash reserve — typically equivalent to 6 months of debt service — held in an escrow account. If the project’s revenues fall short in any period, the DSRA covers debt payments, protecting lenders from immediate default.

Can small and medium enterprises (SMEs) use project finance?

Project finance is generally suited to large capital projects ($50 million+) due to its high transaction costs. SMEs typically use conventional business loans, asset finance, or government-backed programs rather than project finance structures.

What is the Equator Principles framework?

The Equator Principles are a voluntary risk management framework adopted by financial institutions for determining, assessing, and managing environmental and social risk in project finance transactions globally.

What sectors benefit most from project finance in 2026?

Renewable energy (solar, wind, battery storage), digital infrastructure (data centers, fiber networks), and transport infrastructure (roads, rail, airports) are the fastest-growing sectors for project finance in 2026.

What is a waterfall structure in project finance?

A cash flow waterfall defines the strict priority in which a project’s revenues are distributed: first to operating costs, then to debt service, then to reserve accounts, and finally — if all obligations are met — to equity dividends.

What is financial close in project finance?

Financial close is the point at which all financing agreements are executed, all conditions precedent are satisfied, and funds become available for drawdown. It marks the official start of the construction phase.

Conclusion: Project Financing — Building the Future, One Deal at a Time

Project financing is more than a financial technique. It is the mechanism through which societies build hospitals, power the grid, connect cities, and transition to clean energy — without requiring governments or sponsors to bear the full financial burden alone.

In 2026, the fundamentals of project finance remain exactly what they have always been: identify a viable project, structure a bankable SPV, allocate risk appropriately, secure contracted revenues, and attract the right mix of debt and equity. What has changed is the pace, scale, and urgency of the deals — driven by a global energy transition, an infrastructure gap measured in trillions, and institutional capital hungry for stable long-term yields.

For developers, the key lesson is bankability: lenders don’t fund ideas, they fund projects with robust contracts, proven technology, and predictable cash flows. For investors, project finance offers one of the most attractive risk-adjusted return profiles in the asset class universe. For policymakers, it is the most powerful tool available to mobilize private capital for public good.

The world needs more infrastructure than governments can fund alone. Project financing — structured, disciplined, and increasingly innovative — is how it gets built.

About the Author

Javeed Dhillon is a financial writer and infrastructure finance analyst with extensive experience covering project finance, capital markets, and energy investment. His work spans renewable energy, emerging market infrastructure, and structured finance, with a focus on making complex financial concepts accessible to developers, investors, and policy professionals. He writes regularly on project finance trends, deal structures, and bankability frameworks.