FHA Loan 2026: Requirements Current Rates, DTI limit Eligibility & Approval Tips

Article Schema | Type: Article | Author: Javeed Dhillon | Published: April 2026 | Updated: April 16, 2026 | Category: Mortgage & Home Loans |

Primary Keyword: FHA loans | LSI Keywords: FHA loan requirements 2026, FHA loan rates today, how to qualify for FHA loan, FHA vs conventional pros and cons, FHA mortgage insurance, FHA loan limits 2026, government-backed mortgage, first-time homebuyer loan, HUD-approved lender, low down payment mortgage, FHA 203k loan, debt-to-income ratio, mortgage insurance premium. FHA DTI loan limit in 2026.

What Is an FHA Loan?

The Federal Housing Administration loan is a kind of mortgage that the government backs up. The Federal Housing Administration is in charge of this. It is part of the U.S. Department of Housing and Urban Development.

Private lenders that the Federal Housing Administration approves give out these mortgages. The Federal Housing Administration insures them. This means the lender is not taking much of a risk. More people can get a Federal Housing Administration loan. This is especially true for people who do not have credit or a lot of money saved up.

The Federal Housing Administration loan rates today are pretty low. As of April 15 2026 the average rate for a 30-year Federal Housing Administration loan is 6.07 percent to 6.08 percent. This is based on information from Fortune and Optimal Blue. The rate for a 30-year Federal Housing Administration loan is lower than the rate for a 30-year loan. The regular 30-year loan rate is 6.28 percent, to 6.40 percent.

Table of Contents

- What Is an FHA Loan and How Does It Work?

- FHA Loan Requirements 2026 — Full Breakdown

- FHA Loan Rates Today (April 2026) + Rate Forecast

- FHA Loan Limits 2026 by Property Type

- FHA Mortgage Insurance Premiums (MIP) — Full Cost Breakdown

- Types of FHA Loans Explained

- How to Qualify for an FHA Loan: Step-by-Step

- FHA vs. Conventional Loan — Pros, Cons & Expert Opinion

- FHA Loan Application Process

- How to Remove FHA Mortgage Insurance

- FHA Loans for First-Time Homebuyers

- FHA Loan Pros and Cons

- Common Mistakes to Avoid with FHA Loans

- Frequently Asked Questions (FAQ Schema)

- Author Bio

- Conclusion

-

What Is an FHA Loan and How Does It Work?

The Federal Housing Administration (FHA) was established in 1934 during the Great Depression — a period when mortgage defaults were rampant, banks had tightened lending to near-zero, and homeownership rates had collapsed. The government’s solution was elegant: rather than lending money directly, the FHA would insure private lenders against losses if a borrower defaulted. This one mechanism made lenders willing to extend credit to a far broader segment of the American public.

Nearly a century later, the FHA remains the largest insurer of residential mortgages in the world, having backed tens of millions of home loans since 1934. In 2023, an estimated 82% of all FHA purchase mortgages went to first-time homebuyers — a stat that underscores just how central this program remains to the American dream of homeownership.

How the FHA Insurance Mechanism Works

Here is what many borrowers misunderstand: the FHA does not give you a loan. It insures your loan. The money comes from a private lender — a bank, credit union, mortgage company, or online lender. The FHA simply guarantees to reimburse that lender if you stop making payments.

In exchange for this guarantee, borrowers pay mortgage insurance premiums (MIP) — an upfront fee plus monthly charges. This insurance cost is the central trade-off of every FHA loan, and understanding it is essential to making the right mortgage decision.

At-a-Glance: FHA Loan Key Facts (2026)

| Feature | Details |

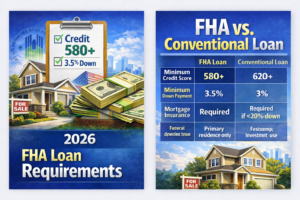

| Minimum Credit Score | 580 (3.5% down) / 500 (10% down) |

| Minimum Down Payment | 3.5% |

| Upfront MIP | 1.75% of loan amount |

| Annual MIP (monthly) | 0.15%–0.55% of loan balance |

| DTI Ratio Limit | 43% standard (up to 50% with compensating factors) |

| 2026 Standard Loan Limit | $541,287 (single-family) |

| 2026 High-Cost Limit | $1,249,125 (single-family) |

| Alaska/Hawaii/Guam/USVI Limit | $1,873,625 |

| Property Type | Primary residence only |

| Available Loan Terms | 15-year or 30-year fixed; ARM options |

| Managed By | U.S. HUD / Federal Housing Administration |

| Regulated Under | HUD Handbook 4000.1 |

-

FHA Loan Requirements 2026 — Full Breakdown

Understanding the full scope of FHA loan requirements in 2026 is critical before you apply. These are the FHA’s baseline rules; individual lenders may add stricter “overlays,” such as requiring a minimum 620 credit score even though FHA allows 580.

Credit Score Requirements

Your FICO score determines your down payment tier:

- 580 or higher → Qualifies for the 3.5% minimum down payment

- 500–579 → May still qualify, but requires a 10% down payment

- Below 500 → Generally ineligible for FHA financing

FHA credit assessment goes well beyond your score number. Lenders also evaluate:

- Your full payment history across all accounts

- Outstanding judgments, collections, and liens

- Bankruptcy and foreclosure history

- Federal debt delinquencies (student loans, taxes)

Even borrowers with thin credit files — those with limited credit history rather than bad credit — can sometimes qualify by demonstrating alternative payment records, such as utility bills or rental history.

Down Payment Requirements for FHA Loans

One of the program’s biggest draws is the 3.5% minimum down payment. On a $300,000 home, that’s just $10,500 — a fraction of the $60,000 required for a 20% conventional down payment.

Crucially, your down payment doesn’t have to come from personal savings.

FHA rules permit funds from:

- Gift money from family members or close friends (must be documented)

- Down payment assistance (DPA) programs from state and local agencies

- HUD-approved nonprofits

- Employer homebuyer assistance programs

This combination of low minimum and flexible sourcing makes FHA loans uniquely accessible for buyers who are cash-constrained.

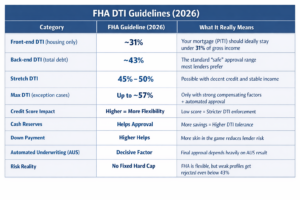

Debt-to-Income (DTI) Ratio

The debt-to-income ratio is one of the most important qualifying factors for any mortgage:

- Front-end DTI (housing costs ÷ gross monthly income): FHA typically wants this at or below 31%

- Back-end DTI (all monthly debts ÷ gross monthly income): Standard maximum is 43%, though lenders can approve up to 50% with strong compensating factors like excellent credit, large cash reserves, or substantial equity

Example: If you earn $6,000/month gross and carry $400 in monthly debt payments (car loan, credit card minimums), your total new mortgage payment including taxes and insurance should ideally not exceed $2,180 to stay within a 43% back-end DTI.

Category |

FHA Guideline (2026) |

What It Really Means |

|---|---|---|

| Front-end DTI (housing only) | ~31% | Your mortgage (PITI) should ideally stay under 31% of gross income |

| Back-end DTI (total debt) | ~43% | This is the standard “safe” approval range most lenders prefer |

| Stretch DTI | 45% – 50% | Possible with decent credit and stable income |

| Max DTI (exception cases) | Up to ~57% | Only with strong compensating factors + automated approval |

| Credit score impact | Higher = more flexibility | Low score = stricter DTI enforcement |

| Cash reserves | Helps approval | More savings = higher DTI tolerance |

| Down payment | Higher helps | More skin in the game reduces lender risk |

| Automated underwriting (AUS) | निर्णायक factor | Final approval depends heavily on AUS result, not just DTI |

| Risk reality | No fixed hard cap | FHA is flexible, but weak profiles get rejected even below 43% |

Income and Employment Verification

FHA requires proof of stable, consistent income. You’ll typically need:

- Pay stubs from the last 30 days

- W-2s from the past 2 years

- Federal tax returns (especially for self-employed borrowers)

- Bank statements from the past 2–3 months

- Self-employed borrowers: profit/loss statements, business tax returns

A two-year employment history is the standard benchmark. Job gaps can sometimes be explained — for example, returning to the workforce after a medical leave or education — but you’ll need documentation.

Property Eligibility Requirements

Not every home qualifies for FHA financing. The property must:

- Be your primary residence (FHA does not finance investment properties or second homes)

- Meet HUD’s Minimum Property Standards (MPS) for safety, security, and structural soundness

- Be appraised by an FHA-approved appraiser who evaluates both value and physical condition

- Be within FHA loan limits for your county

Common property issues that can fail an FHA appraisal include: active roof leaks, exposed wiring, peeling lead paint in pre-1978 homes, cracked foundations, non-functioning HVAC, and lack of working utilities.

Bankruptcy and Foreclosure Waiting Periods

FHA is notably forgiving for borrowers with past financial hardship:

| Event | Waiting Period | Notes |

| Chapter 7 Bankruptcy | 2 years from discharge | Must show re-established credit |

| Chapter 13 Bankruptcy | 12 months of on-time payments | Requires court approval |

| Foreclosure | 3 years from completion | Exceptions for extenuating circumstances |

| Short Sale / Deed-in-Lieu | 3 years typically | May be shorter with extenuating circumstances |

Citizenship and Legal Residency

FHA loans are available to:

- U.S. citizens

- Lawful permanent residents (green card holders)

- Non-permanent resident aliens with eligible visa status and valid Social Security numbers

- DACA recipients (subject to lender policies)

FHA Loan Rates Today — April 2026

FHA loan rates today are among the most competitive in the government-backed mortgage market. Here is the current rate snapshot as of mid-April 2026:

| Loan Product | Average Rate (April 2026) | Source |

| 30-Year FHA Fixed | ~6.07%–6.08% | Fortune / Optimal Blue |

| 30-Year Conventional Fixed | ~6.28%–6.40% | Freddie Mac / Fortune |

| 15-Year Conventional Fixed | ~5.74%–5.80% | Freddie Mac |

| 30-Year VA Fixed | ~5.75% | Rocket Mortgage |

| 30-Year Jumbo | ~6.51%–6.61% | Fortune |

FHA’s rate advantage is real — certain loan types and geographic segments are faring better than others because of lower rates on ARM and FHA loans as well as growing housing inventory in some local markets, according to Joel Kan, deputy chief economist at the Mortgage Bankers Association.

Why FHA Rates Are Often Lower Than Conventional

FHA loans carry a government insurance guarantee, which means lenders face significantly less credit risk. That reduced risk translates to lower base interest rates — especially for borrowers with credit scores below 700, where conventional loans carry significant rate premiums.

However, the APR (Annual Percentage Rate) on an FHA loan is frequently higher than its base interest rate due to the mandatory mortgage insurance premium. Always compare APR, not just interest rates, when evaluating FHA against conventional options.

Rate Outlook for the Rest of 2026

Many forecasts predict mortgage rates will decrease gradually through 2026, though movement is expected to be modest and choppy. The Federal Reserve’s decisions on the federal funds rate remain the biggest wild card. If the Fed cuts rates, FHA mortgage rates could follow. If inflation stays sticky, rates may stay elevated through much of the year.

Expert tip: Even small rate differences compound dramatically over a 30-year loan. Freddie Mac research has shown that borrowers who shop at least three lenders save an average of $600–$1,200 per year on their mortgage.

-

FHA Loan Limits 2026 by Property Type

The FHA sets county-level loan limits annually, adjusted based on local median home prices. For 2026:

| Property Type | Standard (Low-Cost) Limit | High-Cost Area Limit | AK / HI / Guam / USVI |

| 1 Unit (Single-Family) | $541,287 | $1,249,125 | $1,873,625 |

| 2 Units (Duplex) | $693,000 | $1,599,000 | $2,398,500 |

| 3 Units (Triplex) | $837,700 | $1,932,350 | $2,898,500 |

| 4 Units (Fourplex) | $1,040,700 | $2,403,750 | $3,606,250 |

These limits apply to the total loan amount, not the purchase price. In high-cost metro areas — Los Angeles, San Francisco, New York, Seattle, Honolulu — the elevated limits allow FHA borrowers to still access the program without being priced out by local real estate values.

How to find your local FHA limit: Use HUD’s official FHA Mortgage Limits lookup tool at hud.gov to search by state, county, or Metro Statistical Area (MSA).

-

FHA Mortgage Insurance Premiums (MIP) — Full Cost Breakdown

Mortgage insurance is the single most important cost to understand when evaluating an FHA loan. Every FHA mortgage — regardless of credit score, down payment size, or loan amount — carries two layers of mortgage insurance.

Upfront Mortgage Insurance Premium (UFMIP)

- Rate: 1.75% of the base loan amount

- When paid: At closing or rolled into the loan balance

- Example: On a $350,000 FHA loan, UFMIP = $6,125. If rolled in, your starting balance becomes $356,125.

This fee applies to virtually all FHA loan types, including purchase loans, cash-out refinances, and 203(k) renovation loans.

Annual MIP (Charged Monthly)

The annual MIP is divided into 12 equal monthly installments, added to your mortgage payment. The rate varies based on loan term, loan amount, and LTV ratio:

| Loan Term | LTV Ratio | Annual MIP Rate |

| > 15 years | ≤ 90% (down payment ≥ 10%) | 0.50% |

| > 15 years | > 90% (down payment < 10%) | 0.55% |

| ≤ 15 years | ≤ 90% | 0.15% |

| ≤ 15 years | > 90% | 0.40% |

Monthly MIP example: On a $350,000 loan at 0.55% annual MIP = $1,925/year = ~$160.42/month added to your mortgage payment.

How Long Do You Pay FHA MIP?

| Down Payment | MIP Duration |

| Less than 10% | Lifetime of the loan (all 30 years) |

| 10% or more | 11 years |

This is the sharpest distinction between FHA mortgage insurance and conventional PMI. With a conventional loan, PMI automatically cancels when your loan-to-value ratio reaches 80%. FHA offers no such automatic cancellation for most borrowers — which is why refinancing into a conventional loan is a common exit strategy.

True Cost of FHA vs. Conventional MIP Over Time

Scenario: $300,000 purchase price, $10,500 down (3.5%), $289,500 loan amount

| Cost Item | FHA Loan | Conventional Loan (5% down) |

| Down Payment | $10,500 | $15,000 |

| Upfront MIP/Fee | $5,066 (1.75%) | $0 |

| Annual MIP Rate | 0.55% | 0.58% PMI (estimated) |

| Monthly MIP | ~$132 | ~$140 |

| MIP Duration | 30 years | Until 80% LTV (~9 years) |

| Total MIP Cost (30 yr) | ~$47,520 | ~$15,120 |

| Net Difference | Conventional saves ~$32,400 in insurance |

This comparison makes clear: for borrowers who can put 5–10% down with decent credit, conventional often wins on total long-term cost. FHA earns its place when credit scores are too low for competitive conventional rates, or when the down payment is truly limited.

-

Types of FHA Loans Explained

FHA is not a single product. It is a family of programs designed for different needs.

FHA Standard Purchase Loan (Most Common)

This is the core FHA product — a 15-year or 30-year fixed-rate mortgage for purchasing a primary residence. The 30-year fixed is by far the most popular choice, offering the lowest monthly payment. Adjustable-rate FHA loans (typically 5/1 ARMs) are available but far less common.

FHA 203(k) Rehabilitation Loan

The FHA 203(k) loan is one of the most creative and underused tools in residential real estate finance. It allows you to purchase a fixer-upper and finance both the home purchase and renovation costs in a single mortgage — with one closing, one interest rate, one monthly payment.

There are two 203(k) variants:

Limited 203(k) — “Streamline”:

- For cosmetic and non-structural improvements

- Maximum renovation budget: $35,000

- No minimum renovation amount

- Eligible work: flooring, roofing, kitchen/bath remodels, appliances, painting, new HVAC, plumbing updates, accessibility improvements

- No HUD consultant required

- Faster closing than Standard 203(k)

Standard 203(k):

- For major structural repairs (minimum $5,000 in renovation costs)

- No formal maximum renovation cap (bounded by FHA loan limits)

- Can finance: structural reconstruction, foundation repair, room additions, major electrical/plumbing overhauls, septic upgrades

- Requires a HUD-approved 203(k) consultant

- Loan amount based on 110% of property’s after-improved value

- More paperwork; typically 60+ days to close

Both types require licensed contractors and primary-residence occupancy. Luxury upgrades like swimming pools, hot tubs, and outdoor kitchens are explicitly excluded.

FHA Streamline Refinance

If you already have an FHA loan, the FHA Streamline Refinance offers a dramatically simplified path to a lower rate. Key advantages:

- No appraisal required (in most cases) — your loan can even be underwater

- No income or employment verification (non-credit-qualifying option)

- No credit check on the non-credit-qualifying path

- Faster closing with less paperwork

- Potential MIP refund of up to 68% of prepaid mortgage insurance if refinancing within 3 years

- Must deliver a “net tangible benefit” — lower payment, shorter term, or ARM-to-fixed conversion

- Cannot take cash out

FHA Cash-Out Refinance

Homeowners with equity built up in their primary residence can tap it through an FHA cash-out refinance — available whether your current loan is FHA or conventional. The maximum loan amount is 80% of the home’s appraised value. This product is popular for debt consolidation, home improvements, and major expenses.

FHA HECM (Reverse Mortgage)

The Home Equity Conversion Mortgage (HECM) is the FHA’s reverse mortgage program for homeowners aged 62 and older. It converts home equity into tax-free cash (lump sum, line of credit, or monthly payments) with no required monthly mortgage payments. The loan is repaid when the homeowner sells, moves out permanently, or passes away. HECM loans are federally regulated and require mandatory HUD-approved counseling before application.

FHA Energy Efficient Mortgage (EEM)

The EEM program allows borrowers to finance energy-efficient improvements — solar panels, insulation, HVAC upgrades, new windows — into their FHA mortgage amount, even if that amount exceeds the standard FHA loan limit for the area. This loan can be combined with a standard FHA purchase or refinance.

-

How to Qualify for an FHA Loan: Step-by-Step

Knowing how to qualify for an FHA loan requires preparing across multiple dimensions — credit, income, assets, and property. Here is the complete roadmap:

Step 1: Pull and Review Your Credit Reports

Before doing anything else, access your free credit reports from all three bureaus — Equifax, Experian, and TransUnion — at AnnualCreditReport.com. Look for:

- Errors or outdated negative items (dispute these immediately — it can take 30–60 days to resolve)

- Missed payments in the last 12 months (lenders look at recent history most critically)

- Collections or judgments that need to be paid off or addressed

If your score is below 580, you’ll need either a 10% down payment or to spend time improving your credit before applying.

Step 2: Calculate Your Budget

Use an FHA loan calculator to model your total monthly payment, including:

- Principal and interest

- Property taxes (estimated)

- Homeowner’s insurance

- Upfront MIP (if rolling into loan)

- Monthly MIP

Make sure your total housing payment stays within the 31% front-end DTI threshold for your gross income.

Step 3: Save for Your Down Payment and Closing Costs

Even with a 3.5% minimum, you’ll also need closing costs — typically 2%–5% of the loan amount. On a $300,000 purchase with 3.5% down ($10,500), closing costs can add another $6,000–$15,000. Total cash to close: $16,500–$25,500.

Strategies to reduce cash needed:

- Ask the seller to contribute up to 6% toward closing costs (FHA allows this)

- Use a down payment assistance (DPA) grant or second mortgage

- Request a lender credit in exchange for a slightly higher rate

Step 4: Find an FHA-Approved Lender

Not every mortgage lender is FHA-approved. Use HUD’s searchable lender database at hud.gov or ask a real estate agent for referrals. Compare at least three lenders on:

- Interest rate and APR

- Origination fees and closing cost estimates

- Minimum credit score overlay (some require 620 despite FHA’s 580 minimum)

- Customer reviews and average closing times

Step 5: Get Pre-Approved

A pre-approval involves a hard credit pull and submission of your income and asset documents. The lender issues a pre-approval letter stating how much you can borrow — a critical document for making competitive purchase offers.

Step 6: Find a Home Within FHA Guidelines

Work with a buyer’s agent who understands FHA appraisal standards. Avoid making offers on homes with obvious physical defects (roof in disrepair, structural damage, safety hazards) unless you plan to use a 203(k) loan.

Step 7: Complete the Formal Application and Underwriting

Submit the full loan application package with all supporting documents:

- Government-issued photo ID

- Social Security number

- 30 days of pay stubs

- 2 years of W-2s and tax returns

- 2–3 months of bank statements

- Gift letter (if using gift funds for down payment)

- Rental history or mortgage statements (if applicable)

The underwriter reviews your complete file, orders an FHA appraisal, and issues a conditional approval, then a final “clear to close.”

Step 8: Close on Your Home

At closing, you’ll pay:

- Down payment (minus earnest money already deposited)

- UFMIP (unless rolled into loan)

- All remaining closing costs

Sign the loan documents, the deed transfers, and the home is yours.

-

FHA vs. Conventional Loan — Pros, Cons & Expert Opinion

This is the central question most homebuyers face. Let me give you an honest, comparison-based answer — not just a neutral overview, but a real opinion based on the numbers.

Side-by-Side Comparison

| Feature | FHA Loan | Conventional Loan |

| Min. Credit Score | 500 (580 for 3.5% down) | 620 (conventional); 720+ for best rates |

| Min. Down Payment | 3.5% | 3% |

| Mortgage Insurance | Required, all loans | Required only if down < 20% |

| MIP Cancellation | 11 years (10%+ down) or lifetime | Automatic at 80% LTV |

| 2026 Loan Limit | $541,287–$1,249,125 | $832,750 conforming; higher for jumbo |

| Property Type | Primary residence only | Primary, vacation, investment |

| Seller Concessions | Up to 6% | 3%–9% |

| Appraisal Standard | Condition + value | Value-focused |

| Interest Rate (avg) | ~6.07% (30-year) | ~6.28–6.40% (30-year) |

| DTI Maximum | Up to 50% | Up to 45–50% |

| After Bankruptcy | 2 years (Ch. 7) | 4 years (Ch. 7) |

| After Foreclosure | 3 years | 7 years |

FHA vs. Conventional Pros and Cons

FHA Advantages:

- Much more accessible for borrowers with credit scores 500–679

- Lower base interest rates, particularly for below-average credit

- Only 3.5% down payment required

- Gift funds and DPA programs easily accepted

- More forgiving underwriting for past financial hardships

- Sellers can contribute up to 6% toward closing costs — double the typical conventional allowance at lower down payments

FHA Disadvantages:

- Mandatory MIP on every loan, with no exceptions

- Lifetime MIP for borrowers putting less than 10% down

- Restricted to primary residences only

- Lower loan limits in most markets versus conventional conforming

- Stricter appraisal requirements can kill deals in hot markets

- UFMIP adds immediate upfront cost even when rolled in

Conventional Advantages:

- PMI cancels automatically once you reach 20% equity

- Available for investment properties and second homes

- Higher loan limits allow more expensive purchases

- No upfront insurance premium

- Less restrictive property condition requirements

- Better long-term cost for borrowers with 700+ credit scores

Conventional Disadvantages:

- Stricter credit and down payment minimums

- Longer waiting periods after major credit events

- PMI rates can be higher for borrowers with weaker credit

- Less flexibility in accepting seller concessions at lower down payment tiers

Expert Opinion: When Should You Choose Each?

Choose FHA if: Your credit score is below 680, you have less than 10% saved, you’ve gone through bankruptcy or foreclosure in the last 3–7 years, or you need to maximize seller concessions and minimize out-of-pocket costs at closing.

Choose conventional if: Your credit score is 720 or higher, you can put at least 10–20% down, you want to buy a rental property or vacation home, or you want the ability to cancel mortgage insurance relatively quickly.

My honest take: The FHA loan is not a “lesser” mortgage — it is a purpose-built tool for a specific type of borrower. Used correctly (and ideally with a plan to refinance into conventional once equity reaches 20%), it is an excellent bridge to homeownership. Used carelessly — without a plan to exit the lifetime MIP — it can cost borrowers tens of thousands of dollars more than necessary over the life of a 30-year loan.

-

How to Remove FHA Mortgage Insurance

Getting rid of FHA MIP is one of the most frequently Googled questions about this loan type, and the answer is more nuanced than most people realize.

Option 1: Make a 10% Down Payment at Origination

If you put 10% or more down when you first take out the FHA loan, your annual MIP will automatically cancel after 11 years. This is the simplest built-in exit strategy.

Option 2: Refinance Into a Conventional Loan

This is the most common strategy. Once your home’s equity reaches 20% — either through payments, appreciation, or both — refinance into a conventional loan. At that point:

- No PMI required (if equity is already at 20%+)

- No MIP of any kind

- Potentially a lower interest rate if your credit has improved since origination

Example timeline: Buy a $300,000 home with 3.5% down in 2026. Within 4–6 years (depending on appreciation and paydown), you may reach 20% equity. Refinance into a conventional loan at that point and eliminate mortgage insurance entirely.

Option 3: Pay Down the Principal Aggressively

Making extra principal payments accelerates the timeline to 20% equity and positions you for the conventional refinance sooner.

What Does NOT Work

You cannot request MIP cancellation on a 30-year FHA loan with less than 10% down simply by reaching a certain LTV threshold. FHA removed this option for loans originated after June 3, 2013. Prior to that date, MIP could cancel at 78% LTV — but modern FHA loans do not offer this path.

-

FHA Loans for First-Time Homebuyers — Special Considerations

FHA loans are often called “first-time homebuyer loans” — but that label, while common, is technically imprecise. FHA loans are available to any eligible borrower, regardless of whether it’s their first home or their fourth. What’s true is that first-time buyers represent the overwhelming majority of FHA users.

Why First-Time Buyers Love FHA

First-time buyers face a unique set of obstacles: they typically have shorter credit histories, less savings, and less experience with the homebuying process. FHA addresses all three:

- Shorter credit history is acceptable — FHA doesn’t require years of credit depth like conventional lenders sometimes expect

- Low down payment reduces the savings barrier dramatically

- Gift funds are welcome — many first-timers receive help from family

- HUD counseling availability — free HUD-approved housing counseling is available to help first-timers understand their loan options

First-Time Buyer Programs That Layer With FHA

Many state Housing Finance Agencies (HFAs) offer programs specifically designed to complement FHA financing:

- Down payment assistance grants that don’t need to be repaid

- Forgivable second mortgages covering 3%–5% of the purchase price

- Below-market rate first mortgages combined with FHA insurance

- Tax credit programs (MCCs) that reduce federal tax liability

Always check your state’s HFA website and ask your lender about local programs before assuming you need to come up with your entire down payment from savings.

-

FHA Loan Pros and Cons — Honest Summary

✅ Pros

- Lowest credit score threshold of any widely available mortgage program

- 3.5% down payment with credit score 580+ makes homeownership accessible for millions

- Down payment gifts allowed from family, friends, or assistance programs

- Competitive base interest rates, often lower than conventional for credit scores under 700

- Forgiving recovery timeline — eligible just 2 years after Chapter 7 bankruptcy

- Higher seller concessions (up to 6%) help buyers reduce cash to close

- Multiple loan types available: purchase, refinance, renovation, reverse mortgage

- FHA Streamline Refinance allows fast, low-paperwork refinancing for existing FHA borrowers

❌ Cons

- Mandatory mortgage insurance on every loan — no exceptions, regardless of down payment

- Lifetime MIP for borrowers putting less than 10% down (potentially $40,000–$60,000 extra over 30 years)

- UFMIP adds immediate cost — 1.75% upfront on every FHA loan

- Primary residence only — cannot use FHA to buy a rental or vacation property

- Lower loan limits than conventional conforming loans in many markets

- Stricter appraisal standards — homes in poor condition often don’t pass

- APR often higher than stated rate due to MIP stack

-

Common Mistakes to Avoid With FHA Loans

Even with more lenient qualification standards, FHA borrowers can make costly errors. Here are the most frequent pitfalls:

- Ignoring total cost vs. monthly payment: A lower monthly payment from an FHA loan can obscure significantly higher total cost due to MIP. Always calculate total payments over the life of the loan.

- Not shopping multiple lenders: FHA rates and closing costs vary significantly by lender. Studies show shopping at least 3 lenders saves borrowers hundreds to thousands per year.

- Making large deposits before application: Unexplained large deposits in bank accounts trigger underwriting flags. Any funds outside of normal income must be “sourced and seasoned.” Avoid moving large amounts of money in the 60–90 days before applying.

- Opening new credit accounts before closing: New credit inquiries or accounts can lower your credit score and trigger re-underwriting. Freeze new credit applications once you’re in the mortgage process.

- Not considering the FHA 203(k) for fixer-uppers: Many buyers walk away from discounted fixer-uppers because they don’t know the 203(k) exists. If you’re willing to tolerate a longer closing timeline, this program can dramatically expand your options.

- Forgetting about closing costs: FHA’s low down payment is famous, but closing costs (2%–5% of the loan) are a surprise for many first-timers. Factor these in from the beginning.

- Not planning an MIP exit strategy: Taking out an FHA loan without a plan to eventually refinance out of MIP is a mistake for most borrowers. Track your equity and credit score, and be ready to refinance when conditions are right.

-

Frequently Asked Questions (FAQ Schema)

Q: What is the minimum credit score for an FHA loan in 2026?

The minimum is 580 for the 3.5% down payment option. Borrowers with scores between 500 and 579 may still qualify but must put 10% down.

Q: What are FHA loan rates today?

As of April 15, 2026, the average 30-year FHA fixed mortgage rate is approximately 6.07%–6.08%, compared to the 30-year conventional average of around 6.28%–6.40%.

Q: How do I qualify for an FHA loan?

To qualify, you need a minimum 500 credit score, a 3.5%–10% down payment, a DTI ratio under 43% (up to 50% with compensating factors), stable verifiable income, and a property that passes FHA appraisal standards.

Q: What is the FHA loan limit in 2026?

The standard limit for a single-family home is $541,287 in most counties. High-cost area limits reach $1,249,125. Special limits apply in Alaska, Hawaii, Guam, and the U.S. Virgin Islands ($1,873,625).

Q: Are FHA loans only for first-time homebuyers?

No. FHA loans are available to any eligible borrower purchasing a primary residence, whether it’s their first home or a subsequent one.

Q: Can I get an FHA loan after bankruptcy?

Yes. After Chapter 7 discharge, the standard waiting period is 2 years. After Chapter 13, you may qualify after 12 months of successful on-time plan payments with court approval.

Q: What is FHA mortgage insurance (MIP)?

FHA mortgage insurance premiums (MIP) consist of an upfront premium of 1.75% of the loan amount, plus an annual premium of 0.15%–0.55% paid monthly. It protects lenders if borrowers default and is required on every FHA loan.

Q: How long do I pay FHA mortgage insurance?

If your down payment is less than 10%, MIP applies for the full loan term (30 years). With 10% or more down, MIP cancels after 11 years.

Q: Can I use an FHA loan to buy a condo?

Yes, but the condo complex must be on HUD’s FHA-approved condo list or receive individual unit approval. Not all condominiums qualify.

Q: What is the difference between FHA and conventional loans?

FHA loans have lower credit and down payment requirements but carry mandatory mortgage insurance for all borrowers. Conventional loans require stronger credit but allow MIP cancellation and can be used for investment properties.

Q: Can I refinance out of an FHA loan?

Yes. Many borrowers refinance into a conventional loan once they reach 20% equity to eliminate MIP. An FHA Streamline Refinance is also available for existing FHA borrowers seeking lower rates.

Q: What is an FHA 203(k) loan?

The FHA 203(k) is a renovation loan that combines a home purchase (or refinance) with renovation costs into one mortgage. The Limited version covers up to $35,000 in non-structural improvements; the Standard version covers major structural renovations.

Q: Do FHA loans have prepayment penalties?

No. FHA regulations prohibit prepayment penalties, so borrowers can pay off their loan early at any time without fees.

Q: Is the down payment on an FHA loan tax deductible?

The down payment itself is not tax deductible, but mortgage interest and property taxes paid on an FHA loan are generally deductible (subject to IRS rules and current tax law).

Q: Can I use an FHA loan for a multi-family property?

Yes. FHA allows financing for 2–4 unit properties, provided you live in one of the units as your primary residence. The loan limits are higher for multi-unit properties.

-

Conclusion: Is an FHA Loan Right for You?

FHA loans have earned their place as one of the most important tools in American housing finance. They have helped millions of families — particularly those with modest credit, limited savings, or past financial setbacks — access homeownership that would otherwise have remained out of reach.

But they are not the right loan for every borrower. The mandatory mortgage insurance, the lifetime MIP for low down payment borrowers, and the restriction to primary residences make FHA a poor fit for some buyers — particularly those with excellent credit and meaningful savings who could do better with a conventional mortgage.

The honest framework for deciding:

- If your credit score is below 680, or your down payment is under 10%: FHA is likely your best — and possibly only — path to affordable homeownership. Use it, but have a plan to refinance within 5–7 years once equity builds.

- If your credit score is 720 or above and you can put down 10–20%: Run the numbers on both. A conventional loan will almost certainly save you money over the long haul, even if the upfront cost is slightly higher.

- If you’re buying a fixer-upper: Look at the FHA 203(k) before ruling out a property. The ability to bundle purchase and renovation financing can turn a “no” into a “yes.”

- If you already have an FHA loan: The Streamline Refinance is one of the most underutilized tools in real estate. If rates have dropped since you originated, use it.

Whatever path you choose, shop at least three lenders, compare APR (not just rates), and work with a HUD-approved housing counselor if you need guidance. The knowledge you bring to the table is the most powerful tool you have.

About the Author

Javeed Dhillon is a mortgage finance writer and real estate education specialist with over a decade of experience covering government-backed lending programs, homeownership policy, and consumer mortgage markets. His work synthesizes regulatory guidance from HUD, FHA, and CFPB with practical analysis for everyday homebuyers navigating the mortgage process. Javeed draws on primary data from Freddie Mac, Mortgage News Daily, and official FHA publications to ensure every recommendation is grounded in current, verifiable market conditions. He is committed to the principle that informed borrowers make better financial decisions — and that no one should enter a 30-year financial commitment without fully understanding their options.

For feedback, corrections, or topic suggestions, contact the editorial team through the website’s contact form.

References and External Authority Sources

- U.S. Department of Housing and Urban Development (HUD): hud.gov/fha — Official FHA program information and lender database

- Consumer Financial Protection Bureau (CFPB): consumerfinance.gov — Independent consumer guidance on FHA loans

- Freddie Mac Primary Mortgage Market Survey: freddiemac.com/pmms — Weekly benchmark mortgage rate data

- Mortgage Bankers Association (MBA): Industry data on FHA loan origination trends and market share

- FHA Single Family Housing Policy Handbook 4000.1: The regulatory authority governing all FHA single-family programs

- Fortune / Optimal Blue: Daily FHA rate data used in this article’s rate section (as of April 15, 2026)

Disclaimer

This article is for informational and educational purposes only. It does not constitute financial, legal, or mortgage advice. Loan requirements, rates, and limits are subject to change. Always consult with a licensed mortgage professional and HUD-approved lender for guidance specific to your situation. Rate data reflects national averages as of mid-April 2026 and will change over time.